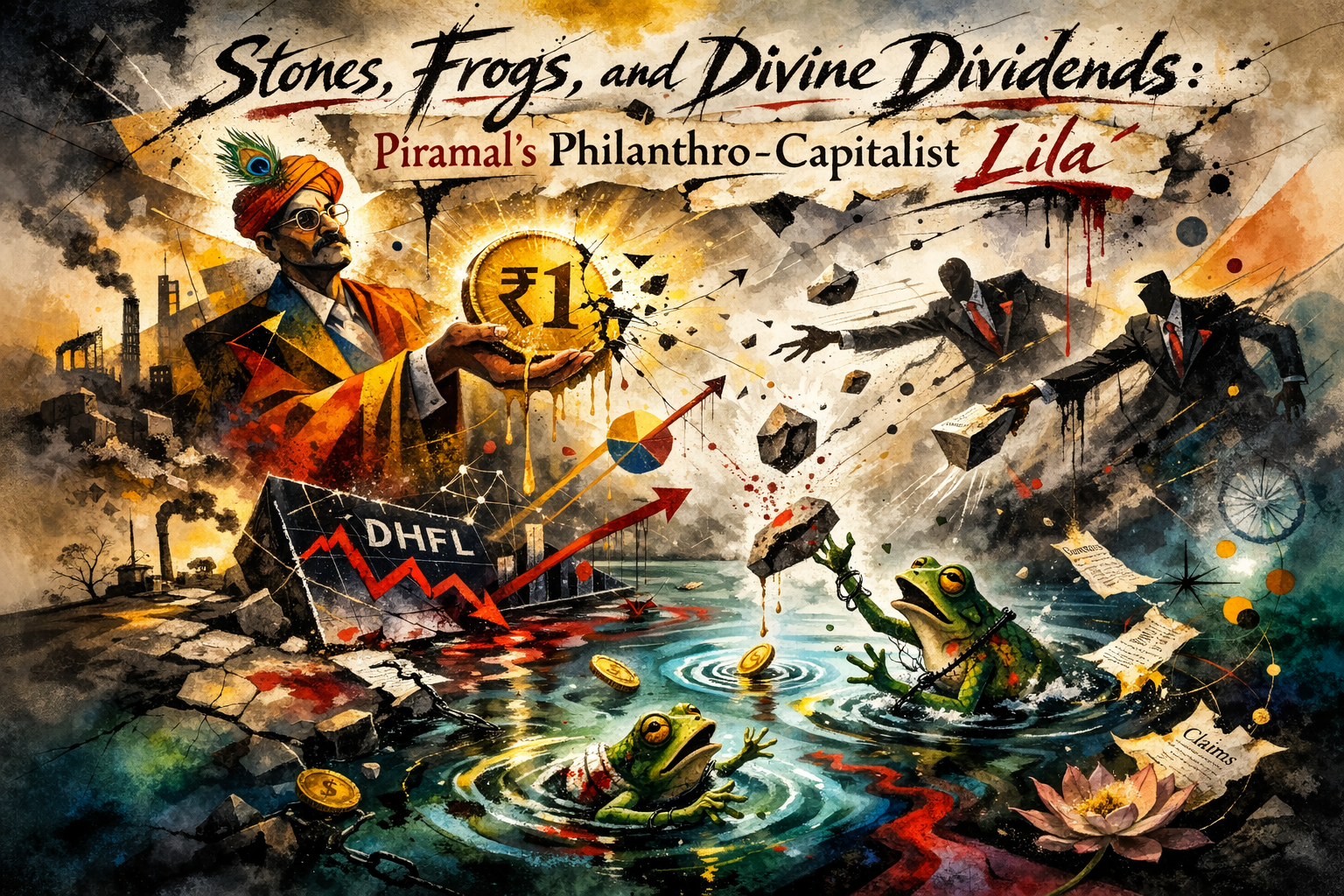

Stones, Frogs, and Divine Dividends: Piramal’s Philanthro-Capitalist Lila

Stones, Frogs, and Divine Dividends: Piramal’s Philanthro-Capitalist Lila

Posted on 22nd February, 2026 (GMT 08:48 hrs)

ABSTRACT

This incisive satirical exposé reinterprets Aesop’s fable of boys throwing stones at frogs as a metaphor for the Piramal Group’s “doing well by doing good” brand of philanthro-capitalism. Blending fable, philosophy, and forensic critique, the piece dissects how corporate strategies cloaked in Vaishnava discourse and Gandhi-branded CSR have enabled empire building that yields profitable acquisitions and regulatory clearance while exacting severe costs from ordinary depositors, small investors, and vulnerable communities. Using the DHFL insolvency resolution as the central case study, it reveals how retail creditors endured steep haircuts, potential fraud recoveries were acquired for a token amount, and corporate reputation was polished through strategic philanthropy and market optics—even as environmental and social harms persist. The narrative extends into allegories of “manufactured trust,” bell-ringing listing galas, and a critique of middle-class apathy framed through the “frog in the well” analogy, arguing that legality, reputation management, and spectacle have substituted for empathy, collective action, and justice. The result is a provocative meditation on late-capitalist finance, moral asymmetry, and the tension between divine metaphor and distributive reality in the Anthropocene of Indian capitalism.

I. Introduction: Welcome to the Privatized Pond

Ah, gentle reader, welcome once more to the pond of contemporaneous mythology—no longer a rustic waterbody fringed with reeds, but a securitized, dematerialized, algorithmically traded system where ancient fables now wear cufflinks. Here, Aesop’s mischievous boys have reincarnated as boardroom barons in bespoke suits, their pebbles upgraded into resolution plans, their laughter transmuted into earnings calls, and their “games” rebranded as strategic acquisitions, distressed-asset optimization, and tax-savvy philanthropy, rather, philanthro-capitalism!

At the shimmering center stands Ajay Piramal: Paramavaishnava industrialist, Gita-quoting executive, Gandhi-invoking empire builder. A man whose public discourse blends Chapter 2 of the Bhagavad Gita with Chapter 11 of the Insolvency and Bankruptcy Code. In this extended satirical meditation—part fable, part philosophy, part forensic capitalism—we explore how the frog’s ancient plea, “What is sport to you is death to us,” evolves into a 21st-century corporate doctrine:

“What is ‘doing well by doing good’ to you is ruin to us.”

Buckle up. The pond has been demutualized. The bell has rung. The frogs remain. Remain vigilant? Vigilant enough?

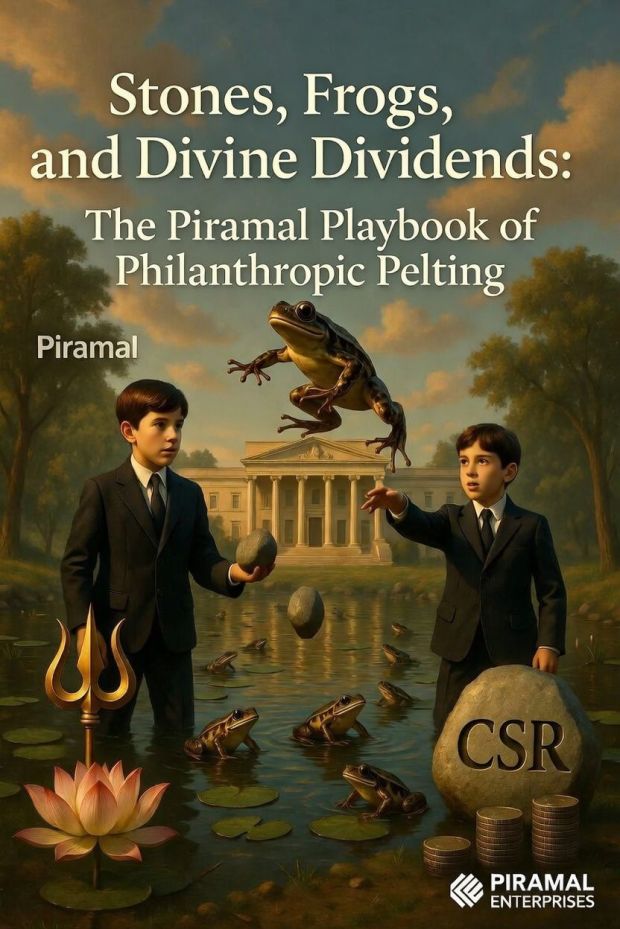

II. From Pondside Pranks to Corporate Carnage: Aesop Revisited with Audit Trails

Let us return to the original Aesop’s fable, that ancient Greek moral vignette: The Boys and the Frogs.

A group of boys gather at a pond. They throw stones at frogs for amusement. Some frogs die. One brave frog rises and pleads:

“Pray stop, my boys: what is sport to you is death to us.”

The boys, struck by conscience, desist. Moral clarity prevails.

The genius of this fable lies in perspectival ethics. The asymmetry between intention and impact. Between play and annihilation. Between boredom and extinction. It teaches empathy across power gradients.

But what happens when the boys grow up?

What happens when the stone becomes a structured financial instrument?

When the pond becomes a balance sheet?

When the frog’s death becomes a “haircut”?

The ancient fable assumed shame was possible. Our contemporaneous variant tests whether reputational management can substitute for remorse.

III. Pelting with Purpose: Piramal’s Chaosophic Casino Capitalism

Enter the doctrine: “Doing well by doing good.”

A phrase so elegant it dissolves contradiction. A slogan that makes profit appear as philanthropy’s twin flame.

In this upgraded pond, the frogs are no longer amphibians. They are DHFL fixed deposit holders, non-convertible debenture investors, pensioners, widows, small savers—the quiet citizens who believed in AAA ratings and housing-finance stability.

Then came a forced insolvency as a “litmus test”. Frogs became guinea pigs.

DHFL—once a ₹94,000+ crore claims labyrinth—got surgically sliced and handed to Piramal for ≈₹34,250–37,250 crore under the IBC’s sacred “value maximization” altar. Retail FD holders and small NCD investors? They swallowed 40–60% recoveries (often plunging into 55–77% effective haircuts, leaving grandma’s life savings in tatters). Big banks nodded along with their “commercial wisdom.”

And the pièce de résistance? Those juicy ~₹45,000 crore in avoidance/fraudulent transaction claims—diverted loans, shell-company round-tripping, promoter siphoning galore—were casually valued at a majestic Re 1 in the Piramal resolution plan. Yes, one solitary rupee.

Supreme Court, in its April 2025 wis(h)dom (upholding the plan and overruling NCLAT qualms), graciously ruled that any future recoveries from those Section 66 fraudulent/wrongful trading goodies belong exclusively to Piramal (now Piramal Finance, post-reverse-merger glow-up). Not a paisa back to the bleeding creditors. Clean slate for the acquirer, permanent red ink for the retail victims. Red ink turning April 1 into a red letter day!

So, in one IBC masterstroke: Piramal effectively scooped up a potential ₹45,000 crore treasure chest of fraud recoveries for literally 1 rupee, while lakhs of middle-class depositors watched their fixed deposits evaporate into “haircut” folklore. Value maximization achieved. Commercial wisdom prevails. Death of retail trust? Just another Tuesday in India’s insolvency theatre.

And who emerged triumphant?

The acquiring entity, Mr. Piramal—integrated, expanded, rebranded, reverse merged — potentially to cunningly disown past accountabilities. Suddenly among India’s largest housing finance players. Assets under management surged. Low-coupon debentures sweetened capital structures. The balance sheet gleamed.

The frogs? They were told the process was legally sound. The Supreme Court affirmed binding finality in 2025. The game was valid. The sport was lawful.

But Aesop’s frog was not asking about legality.

He was asking about empathy.

IIIA. CSR as Consolation Prize

Enter the philanthropic overlay:

Healthcare helplines.

Education initiatives.

Water kiosks.

Youth fellowships.

Rural transformation labs.

All admirable in isolation. All tax-deductible in structure. All strategically communicable.

Because in late capitalism, philanthropy does not follow profit—it often legitimizes it.

The paradox sharpens to razor-edged irony in Piramal’s post-DHFL empire: billions were “saved” through those legendary haircuts that carved deep into retail pockets—tens of thousands of crores shaved off admitted claims while the acquirer pocketed the upside of undervalued fraud recoveries and future windfalls—all neatly wrapped in IBC’s value-maximization gospel.

Yet, millions flowed generously into CSR coffers year after year—tens of crores dutifully spent on healthcare, education, tribal upliftment, green(-washed) projects, and “doing well by doing good” initiatives, proudly paraded in sustainability reports and awards as proof of benevolent capitalism.

Reputation? Compounded handsomely: stock narratives polished, demergers celebrated as strategic genius, Davos sages nodding at purposeful lending, while critics’ whispers of crony cunning and depositor devastation got drowned out by fresh branch networks, retail AUM explosions, and philanthropic glow-ups.

And the moral arithmetic? Perfectly balanced on the ledger of selective compassion—where massive creditor losses become efficient restructuring, one-rupee asset grabs turn into smart acquisitions, and token millions in charity wash away the billions extracted from the very middle-class savers the system claims to protect. In this grand theatre of Indian insolvency, the books close spotless: profits privatized, pain socialized, virtue signalled, and equilibrium restored—one paradoxical rupee at a time.

The frog croaks again:

“What is ‘doing well by doing good’ to you is ruin to us.”

But the pond has new management. And the annual report glows.

IV. “Buy Imperfect, Sell Perfect”: The Gospel According to the Boardroom

Ajay Piramal’s oft-cited mantra—“Buy imperfect, sell perfect”—is celebrated as strategic brilliance.

Let us admire its elegance.

- Acquire Distress:

Buy entities tainted by fraud, regulatory probes, governance failure.

DHFL is the exemplar: distressed, discredited, discounted. - Integrate & Rebrand:

Invoke IBC’s “clean slate” doctrine.

Demerge. Reverse merge. Rename.

Scrub legacy baggage via statutory purification. - Monetize Renewal:

Present refreshed ticker symbols.

Ring exchange bells.

Project ₹1.5 lakh crore AUM ambitions by 2028.

Imperfection becomes arbitrage.

But perfection for whom?

For shareholders?

For brand equity?

For regulatory optics?

Not for the frog who entered under AAA illusions.

IVA. Digwal, Real Estate, and Sanitized Sites

The paradox sharpens into a full-blown corporate tragicomedy across Piramal’s empire, where toxic legacies and climate gambles get effortlessly laundered into saintly CSR spotlights and swift regulatory reprieves. Polluted industrial landscapes—like the decades-long groundwater nightmare in Digwal, near Hyderabad, where pharmaceutical effluents have turned wells undrinkable, crops barren, and villagers chronically ill since the 1990s (with fresh NGT petitions in 2024 alleging ongoing discharges despite past “resolutions”)—magically transform into heartwarming CSR tales of community health centers, RO Water ATMs, upliftment drives, and “sustainable” green initiatives proudly splashed across annual reports.

Contested pharmaceutical effluents reach peak absurdity in Dahej, February 2026: a tanker allegedly dumps spent hydrochloric acid into a Narmada-linked canal (Gujarat’s lifeline for millions), triggering an immediate GPCB closure order under Section 33A, a ₹1 crore environmental compensation slap, Supreme Court scrutiny (with CJI bluntly noting the risk to public water sources), and a swift interim revocation by mid-February allowing ops to restart—neatly counterbalanced, of course, by clean-water kiosks, safe-drinking campaigns, and “hydration for aspirational districts” spends that make the occasional acid detour look like a minor operational hiccup in the grand narrative of responsible pharma.

Flood-prone luxury towers sprout shamelessly in Mumbai’s most vulnerable coastal lowlands—Piramal Mahalaxmi perched at 3–5 meters above sea level in Jacob Circle, Piramal Vaikunth gnawing into Thane Creek mangroves—hawked as aspirational biophilic havens with “panoramic lifetime sea views” and resilient luxury vibes, even as Climate Central and IPCC projections flag accelerating inundation, king-tide submersion, and routine flooding by 2050 under modest sea-level rise. Buyers get today’s skyline glamour; tomorrow’s taxpayers foot the bill for rescues, pumps, and inevitable bailouts when the Arabian Sea claims its due.

Electoral bonds? Those now-defunct but eternally instructive proximity plays quietly greased the wheels—reports of ₹85 crore+ funneled to the ruling party via bonds (pre-ban) aligning suspiciously with policy windfalls, regulatory soft-landings, and expansion green lights—ensuring that enforcement theatre (closures, notices, observations) resolves into operational normalcy faster than you can say “interim revocation.”

In Piramal’s masterclass of sanitized capitalism, the moral arithmetic balances with surgical precision: ecological poison and public-health externalities offloaded onto marginalized villagers, downstream communities, and future flood victims; profits, stock rallies, and philanthropic PR compounded privately; virtue broadcast loudly through crores in CSR while billions in avoided liabilities and one-rupee windfalls stay pocketed. From Digwal’s slow poison to Dahej’s quick acid detour to Mumbai’s rising climate time-bombs—the pattern repeats with flawless impunity: violate boldly, face brief regulatory drama, normalize swiftly, narrate nobly, and repeat. One rupee recoveries here, billions extracted there, millions “given back” in charity—equilibrium restored, corporate conscience clear, public burden eternal.

Imperfection purchased.

Perfection narrated.

The Gita quoted.

The spreadsheets reconciled.

V. Bell-Ringing and Bitter Bubbles: The Listing Gala

Ah, croak if you’ve heard this one before: while the boys in the boardroom upgrade their stone-pelting to bell-ringing, the frogs of the pond—those beleaguered 98%, the small investors still licking wounds from DHFL haircuts—peer through the gilded gates at yet another ostentatious spectacle. Enter the grand inauguration of Piramal Finance Limited’s stock exchange listing, a November 7, 2025 extravaganza at Mumbai’s NSE headquarters, where the chaosophic casino hits jackpot levels of irrationally rational excess.

Picture this: Ashishkumar Chauhan presiding like a high priest, Ajay Piramal beaming in bespoke attire, and the Ambani clan—Isha Ambani (fresh from her own twin-birth opulence), Radhika Merchant, Shloka Mehta, and matriarch Nita Ambani—gracing the affair like royalty at a merger-made marriage. Soulful melodies curated by “The Event Co.” fill the air, perhaps a nod to Ramanuja’s divine lila, but really just elevator music for empire expansion as the NSE bell tolls for a refreshed ticker symbol, post-DHFL integration and demerger.

From my lily pad vantage—displaced by rising waters and falling recoveries—this “gala” unfolds as a risky space of money-signifiers begetting more money-signifiers, bullish or bearish depending on whose pond you’re in. Game theory presumes rational agents; yet here we are in Guattari’s delirious market. The tycoon boys bet big on “buy imperfect, sell perfect,” flipping fraud-tainted assets into AUM glory (targeting ₹1.5 lakh crore by 2028, no less), while we frogs “rationally” deposited savings lured by AAA illusions, only to get pelted with 55–77% losses.

Irrationally rational, indeed. Why participate? Because the game’s rigged by rating agencies peddling “manufactured trust,” brand ambassadors sprinkling stardust, and watchdogs like SEBI and RBI dozing through the chaos—enforcing oligopolies where signals dilute and scrutiny defers.

Echoing that fox’s tale of sour grapes at the Ambani-Piramal wedding vineyards—where weddings devour billions amid hunger, and U.S. births hedge privileges for the unborn scions—this frog witnesses a corporate birth: Piramal Finance emerging pristine from DHFL’s imperfect carcass, celebrated with chartered cheers and investor calls (January 20, 2026, for good measure).

The 98%? We’re the displaced, clutching fences while the 2% feast on enclosures—Antilia-high and Gulita-secure—preaching Atmanirbhar Bharat but ringing bells for crony windfalls. Grapes? Always sour down here. This lila’s “divine play” is just another spin of the wheel, where our existential splatter funds their philanthropic fireworks.

Croak on, comrades—pass the pond scum, for the house always wins.

VI. Manufactured Trust and the Oligopoly of Belief

Credit rating agencies—CRISIL, ICRA, CARE—function within issuer-pays architectures. Surveillance ratings cluster at the upper tiers for powerful issuers. Downgrades often arrive post-default.

Manufactured trust lubricates capital flows.

Brand ambassadors add narrative sheen.

SEBI imposes procedural penalties.

SAT often mitigates them.

RBI monitors systemic stability while socialized losses cascade downward.

The frog does not understand basis-point spreads.

He understands only that his nest egg dissolved.

VII. Ramanuja’s Lila vs. Corporate Lila 2.0

Let us now ascend to metaphysics, theology—though in the boardroom, it’s more like a quarterly earnings call disguised as enlightenment.

In Visistadvaita, Ramanuja’s lila is divine play without ulterior motive, a concept meticulously unpacked in his Sri Bhasya commentary on the Brahma Sutras. Here, Saguna Brahman—the qualified Absolute, brimming with attributes like omniscience, omnipotence, and infinite bliss—engages in world-creation not from any deficiency or cosmic boredom, but as an overflow of sheer ananda (bliss). Think of it: Brahman, already purna (full), doesn’t “need” to create; He sports (lila) freely, manifesting the universe as His own body (sharira), where souls and matter are inseparably dependent modes (prakaras) of His essence. No extraction, no hidden fees—just incidental harmony, where the world’s sustenance flows from divine grace like an unasked-for bonus, diffusing equitably without a shareholder vote.

Contrast this with Corporate Lila 2.0, where the CEO plays god in a pinstripe suit:

Acquisitions framed as destiny—because swallowing competitors is just Saguna Brahman’s way of “expanding the body,” right?

Losses framed as inevitability—externalized costs dumped on the proletariat, while executives cite karmic cycles to justify golden parachutes.

CSR framed as grace—a tax-deductible dribble of philanthropy, masquerading as diffused ananda, but really just PR for the next round of profit-hoarding.

Electoral proximity framed as civic contribution—lobbying as lila, where “divine play” means rigging the game for favorable regulations.

The Gita’s verse (2:47) on detachment from fruits is recited in mindfulness retreats for stressed VPs.

Yet fruits appear in quarterly earnings, ripe and taxable only for the underlings.

The frog revises scripture—croaking from its lily pad throne: “You may perform your prescribed duties—but we bear the fruits, and invoice you for the privilege.”

Ramanuja’s cosmos benefits incidentally from divine sport, where Saguna Brahman’s lila ensures that creation’s purpose is self-delight, not self-enrichment, with grace permeating all jivas (souls) without a means test or NDA.

The corporate cosmos benefits selectively—gains concentrate in offshore accounts, while the “body” of the company sheds workers like autumn leaves, all in the name of “optimizing the prakaras.”

In one, grace diffuses like sunlight on a Ramanujan theorem—universal, unearned, unmanipulated.

In the other, it trickles down like executive bonuses: concentrated, conditional, and always with strings attached. Ah, the bliss of late capitalism’s twisted Vedanta.

In the other, gains concentrate.

VIII. Sour Grapes and Antilia-Gulita Heights

From Antilia to Gulita, from chartered births abroad to wedding feasts devouring billions, spectacle becomes governance’s twin.

The 2% celebrate listings.

The 98% clutch recovery slips.

The fox declares grapes sour.

The frog declares the pond privatized.

Both are dismissed as envious.

Yet envy is not the issue.

Asymmetry is.

IX. Rational Frogs in an Irrationally Rational Arena

Why did investors deposit in DHFL?

- High yields.

- AAA ratings.

- Regulatory legitimacy.

- National housing narrative.

- Implicit trust in systemic oversight.

Optimism bias met structural opacity.

Game theory with its “rational choice” presumes informed agents.

Chaosophy reveals subjectivity engineered by capital flows.

The frogs were not foolish.

They were structurally positioned.

The boys were not irrational.

They were systemically advantaged.

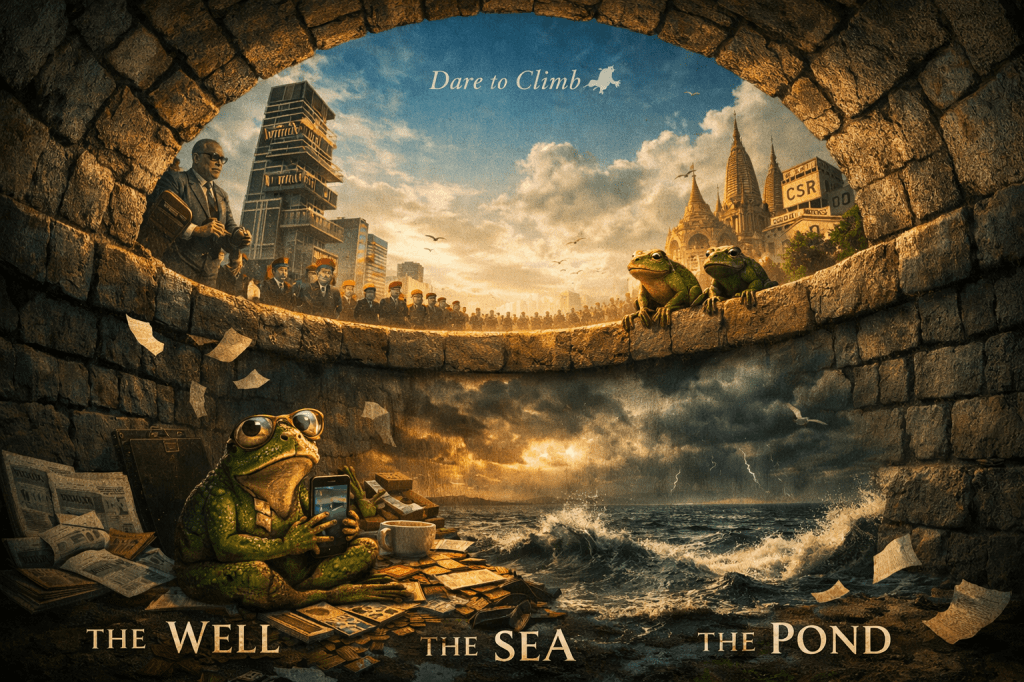

X. Frog in the Well: Middle-Class Myopia and the Geometry of Apathy

Permit one final amphibian allegory before we drain this pond.

If Aesop gave us the frog beneath the stone, the subcontinental archive offers us another creature: the frog in the well—kuan ka mendak—that legendary provincial philosopher who mistakes the circular sky above his well for the entirety of existence. When the sea-frog visits and speaks of oceans, tides, and vastness, the well-frog laughs, incredulous, secure in the circumference of his masonry world.

Our DHFL frogs, let us admit with discomfort, were not merely pelted.

Many were such well-frogs.

The frog in the well

measures the sky

by the circumference of habit.

EMIs for horizon.

WhatsApp for weather.

Ratings for scripture.

When the sea-frog speaks of tides,

he calls it exaggeration.

When the stone falls,

he calls it fate.

But wells do not protect.

They contain.

Climb.

#FrogInTheWell, #MiddleClassApathy, #EducateAgitateOrganize, #OrganizeForJustice, #VictimsUnited, #CivilDisobedience, #Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion, #Seize_Cronies_Fairplay_for_DHFL_Victims,

The Indian middle class—educated, credentialed, salaried, digitally connected—occupies a peculiar epistemic well. It is lined with EMIs, SIPs, LIC policies, school admissions, gated societies, cheap WhatsApp University forwards, and the fragile pride of “respectability.” The sky it sees is curated: credit ratings, annual reports, televised debates, Davos photo-ops, CSR documentaries, temple donations, and the reassuring mantra that “the system ultimately works.”

When the sea roared—when whistleblowers cried fraud, when investigative journalists flagged accounting contortions, when NCLAT murmured dissent before being overruled—most well-frogs did not leap outward. They refreshed their apps. They trusted procedure. They awaited judicial salvation.

And when the haircut arrived?

There was outrage in drawing rooms.

There were uncoordinated murmurs in Telegram groups.

There were petitions signed, though in a dispersed manner.

There were strongly worded emails.

But no sustained non-violent civil disobedience, as OBMA always attempted to perform.

No cross-class solidarities.

No occupation of regulatory sidewalks.

No coordinated depositor unions occupying public squares.

The well remained intact.

Why?

Because the Indian middle class is structurally fragmented—linguistically, caste-stratified, regionally siloed, ideologically polarized. Because its technological fluency produces clicktivism rather than collectivism. Because it fears reputational risk more than financial ruin. Because it has internalized the theology of procedural faith: courts will fix it; regulators will act; markets will self-correct; karma will balance.

And because, crucially, it still aspires upward.

The well-frog does not revolt against the boys;

it hopes to join them, in fear, in blind obedience.

Thus apathy is not mere laziness. It is aspirational alignment. The middle class imagines proximity to Antilia more than solidarity with the dispossessed. It fears sliding downward more than it resents extraction upward. It distrusts street politics. It equates protest with instability. It calls dissent “anti-development.” It whispers about “maintaining decorum.”

Technophobia plays its quiet role too. Complex insolvency codes, Section 66 proceedings, forensic audits, reverse mergers—these appear arcane, best left to experts. “Too complicated,” says the well-frog, retreating to devotional YouTube channels and mutual fund or share market webinars. The architecture of financial opacity becomes an anesthetic.

And so the privatized pond persists.

The boys ring bells.

The CSR videos circulate.

The regulators issue notices.

The Supreme Court affirms finality.

The balance sheets reconcile.

Meanwhile, the well-frogs debate morality in private, grieve losses quietly, and recalibrate portfolios with stoic resignation.

The tragedy is not only that stones were thrown.

It is that the frogs did not swarm.

For had the well-frogs recognized themselves as oceanic—crossing caste, profession, religion, ideological camp and WhatsApp echo chambers—they might have transformed isolated croaks into a chorus capable of unsettling the boardroom acoustics.

Instead, they adjusted.

In Aesop’s tale, shame stopped the boys.

In ours, legality shields them.

And well-frogs, mistaking the circular sky for justice, console themselves with dividends yet to come.

The pond is privatized.

The well is self-contained.

The sea waits.

Croak—if you dare to climb.

XI. Conclusion: The Privatized Moral

And so the last stone skips.

The pond is securitized.

The bell has rung.

The ticker trades.

The CSR brochure glows.

Aesop’s original tale ended with shame and reform.

Our version ends with listing gains and dividend yields.

The moral, revised for the Anthropocene of finance:

- Legality is not empathy.

- Resolution is not restoration.

- Philanthropy is not absolution.

- Divine metaphors do not erase distributive asymmetry.

Ramanuja’s lila was cosmic compassion.

Corporate lila is leveraged choreography.

The frog still croaks:

“What is divine sport to you is existential splatter to us.”

Hari Om.

Pass the merger documents.

And may your investments fare better than a DHFL frog.

Comments

Post a Comment