Piramal’s Fixated Obsession with Re 1: Documentation, Con-figured Equivocation and the Facade

Piramal’s Fixated Obsession with Re 1: Documentation, Con-figured Equivocation and the Facade

Posted on 27th February, 2026 (GMT 07:28 hrs)

ABSTRACT

Written from the standpoint of one pauperised by the DHFL collapse—once a trusting fixed-deposit holder, now among the dispossessed—this essay interrogates Piramal Finance’s “Neeyat” campaign as an apparatus of aggressive linguistic marketing that weaponizes micro-honesty to legitimize macro-consolidation. Through semiotic, Marxian, psychoanalytic, and political-economic analysis, it traces how the repeated invocation of Re 1—returned in scenes of everyday virtue (a coin handed back, a packet retrieved, kinship invoked)—operates as myth: at the level of denotation, simple integrity; at the level of connotation, character over paperwork; at the level of ideology, ethical finance naturalized precisely after an insolvency process in which avoidance claims worth approximately ₹45,000 crore were assigned a notional value of Re 1 and retail creditors absorbed devastating haircuts under the shelter of IBC jurisprudence and Section 32A immunity. The same rupee circulates across regimes—as legal token, advertising prop, and ideological shield—while high-yield lending, SARFAESI enforcement, ratings upgrades, and judicial deference to “commercial wisdom” consolidate capital. Self-reflexively acknowledging its wounded vantage, the essay reads the compulsive return of Re 1 not as branding ingenuity but as symptomatic spectacle: a coin endlessly restored on screen while restitution remains foreclosed in law, revealing how moral minimalism at the micro level masks structural dispossession at the macro level.

In Continuation With

I. Introduction

I write to all; I write to each.

As a DHFL victim turned into a pauper, I am no longer able to survive on my scanty savings. Most of my savings were engulfed in the aftermath of what has come to be designated as the “DHFL scam.” I believed the auditors’ glowing reports. I retained faith in the AAA credit ratings. I believed in SRK’s brand advertisements. All of these deceived me, duped me, misled me. My money was taken through a “resolution process” and a “resolution plan” of Mr. Ajay Piramal—taken to be a great philanthropist—yet his settlement proposal did something that never enabled most of our invested money to return to us. That “something” has been called by some to be an act of expropriation, dispossession, and disenfranchisement, reportedly supported (or, actively aided) by the state–corporate machinery within which today’s India under the BJP rule is suffering.

I unlock my smartphone. Open the YouTube app. Start scrolling. I do not know why, but a thought crosses my mind. I type “Piramal Finance ads” into the taskbar.

I encountered three consecutive advertisements, which I describe below.

Since early 2023, Piramal Finance has saturated Indian screens with the “Neeyat” campaign—a multi-phase emotional juggernaut conceptualised by The Womb agency. The unchanging core slogan remains: “Hum kagaz se zyaada, neeyat dekhte hain.” “We look at intent/integrity more than papers.” Three foundational ad-films established the emotional grammar, and later iterations (Neeyat 2.0, Neeyat 3.0, and the “Neeyat se banaya hai, neeyat se badhoge bhi” Diwali specials in late 2025) have only intensified this pre-fed pattern.

I watch them closely now. I watch them care-fully.

Ad 1 (setting the scenes)— A nervous blacksmith confesses he lacks formal income documents needed to take a loan. The Piramal executive, radiating manufactured benevolence, waves the concern away: “Sir, we have verified… whether you took one lakh rupees or even one rupee, you have always repaid it. You will get the loan. We value integrity more than paperwork (hum kagaz se zyaada neeyat dekhte hai).”

Link: https://youtu.be/Oz0-vA4c_yc

Ad 2 (the signature piece, still in heavy rotation) — A customer hands over a ₹500 note for an item priced at ₹499. The shopkeeper, glowing with virtue, returns the extra rupee with theatrical warmth: “Areh, Bhaisaab—499!” The voice-over once again delivers: “Neeyat sahi par kuch kagaz nahin? Loan ke liye, aaiye baat karte hain!” Honesty is proven in what you return, not what you keep? Really?

Link: https://youtu.be/sn2IG9ht0GU

Ad 3 (Marathi version, but speaks to all) — A delivery-person/supplier with a cycle walks past a security guard; a snack packet slips from the cycle’s handlebars and falls unnoticed. The guard bends, picks it up, runs after the vendor and calls, “Kaka!” They exchange smiles as the packet is returned. Fade to slogan (in translation to Hindi): “Neeyat sahi, par kagaz-patra nahin… aaiye baat karte hai.”

Link: https://youtu.be/O9Z6vrdFgTA

The message in each and all is evangelical and inescapable: Piramal Finance is the empathetic disruptor that trusts character over bureaucracy, the lender that returns what is not theirs, the bank for India’s vast informal economy long rejected by rigid traditional institutions.

This is not subtle positioning. It reads instead as aggressive linguistic marketing—obsessive and repetitive, arithmetically fixated on a single symbolic figure: Re 1. Alongside this fixation runs the performative gesture of “returning” what was never legitimately one’s own, entangled with the question of kagaz—the fraught politics of documentation, proof, and bureaucratic legitimacy.

Well, well, well.

I lock my smartphone and set it aside.

I try to sit with these ads. To truly delve into what they are. What are they trying to say, trying to convey? What are they promoting, and what has Piramal Finance been doing all along? What do the facts say? How do these ads manufacture parallel, alternate irrealities—irrealities that are extremely real to the target consumer—but to a DHFL victim like me, through my own lensing, render me uncomfortable, unsettled?

The more I replay them, the more I notice not just the message—but the repetition.

Re 1.

Returned.

Remembered.

No need for documents….?!

Reperformed.

There is a propaganda principle often attributed to Goebbels: repeat some lie often enough and it begins to harden into truth. I am not equating contexts; I am observing mechanism. Repetition does not argue—it saturates. The rupee becomes less currency and more incantation. Each small restitution overwrites larger absences. Each returned coin quietly suggests institutional innocence.

And then McLuhan echoes: the medium is the message.

These are not print disclosures buried in annual reports. They are digital ad-films—warm, intimate, algorithmically circulated, endlessly replayable. In electronic capitalism, affect travels faster than audit. A ₹1 gesture fits perfectly into a reel. Structural magnitude does not.

The medium compresses morality into micro-scenes: a coin returned, a promise delivered, a packet retrieved, trust affirmed. Re 1 in the projected absence of paperwork becomes a moral unit of measurement. Integrity is miniaturised, cinematic, shareable.

Repeat the rupee enough times, and perception reorganises itself around it.

What unsettles me is not what the ads say—but what their repetition, and their medium, allow us to forget.

Some problem-questions bombard my already crippled mind.

I write down a few of them here.

Setting the Scenes Without Drawing the Drapes:

Key Problem-questions

About Ad Video 1

A. A loan without any paper? How can that be possible? What do the governing rules, regulatory frameworks, and compliance norms actually stipulate? Is this rhetoric, or is there a regulatory elasticity being invoked?

B. Who precisely are the (soft) target consumers—the informal sector, the unorganized workforce, those lives and labours that rarely get absorbed into the statistical triumphalism—the fascism—of GDP accounting? Why are they selected as the primary audience? Are they being positioned as beneficiaries of inclusion, or as vulnerable terrains for corporate predation?

C. If PMAY (Pradhan Mantri Awas Yojana) exists as a state-backed housing scheme under the BJP, why are daily wage-earners/poor labourers turned into borrowers compelled—or persuaded—to seek housing loans from a private financial entity instead? What structural gap is being filled here, and at what cost?

D. Why should I take a loan from an institution whose principal figure is himself burdened with significant market debt, given Piramal’s substantial financial liabilities in the market as they stand today? What does indebtedness mean when the creditor is also deeply indebted?

E. Is Piramal Finance operating as a “Double Dealer”—performing ethical populism in its advertisements while navigating a different arithmetic in its reported financial conduct over the years?

F. How does one equate “1 rupee with 1 lakh rupees”, or how could one equate Rs. 10 with a bottle of water—how does one standardize value, dignity, survival, into such neat transactional metaphors, structurating inequals into equals?

About Ad Video 2

A. Returning Re 1—juxtaposed with DHFL’s ₹45,000 crore worth of assets valued at Re 1 for Mr. Piramal. Is this a double standard? Or a choreography of moral symbolism? What is the psychoanalytic underpinning of this?

B. What explains Piramal’s near-obsessive return to the figuration of Re 1? Is there an obsessive moral arithmetic at play—Piramal Finance’s ritualistic invocation of Re 1 as a spectacle of integrity, while larger sums dissolve into abstraction?

About Ad Video 3

A. If the security guard in the advertisement is portrayed as the ethical custodian—dutifully returning a fallen snack packet of snacks as a symbol of everyday honesty—how do we reconcile this with the unaccountable gatekeepers of the DHFL resolution process? While the guard safeguards trivial property with moral sincerity, the lifetime savings of DHFL depositors—absorbed through a controversial resolution framework—remain unrestored. Does this contrast expose a troubling double standard? Or does it point toward a deeper institutional hypocrisy?

B. More critically, does the advertisement manufacture a spectacle of integrity by foregrounding the moral virtue of a powerless guard, while the actual gatekeepers of financial power remain insulated from scrutiny? In other words, are we witnessing a carefully staged morality play—where symbolic micro-honesty is dramatized, even as structural dispossession and fiduciary opacity go unaddressed?

Taken together, does this recurring invocation of “Re 1” not begin to resemble more than an engineered motif? It appears less like coincidence and more like fixation—a symbolic condensation of value, virtue, and transaction into the smallest possible unit of currency. Why this relentless return to the minimal denomination? Why must integrity be staged through the theatre of the negligible?

Does such repetition merely simplify a message for mass recall, or does it rehearse a deeper logic—one in which magnitude is morally neutralised and enormity is rendered abstract? When colossal restructurings are narrativised through the language of tokenism, when vast financial rearrangements are shadowed by the rhetoric of the infinitesimal, what kind of arithmetic is being performed?

Is this the grammar of supplementation—where the smallest coin becomes the emblem of righteousness, and the scale of consequence quietly recedes from view? Or is it simply branding—nothing more, nothing less?

I pause.

I let the number hover.

And I attempt, once again, to descend beneath the surface of these ad-films.

DHFL’s ₹45,000 crore reduced to Re 1 — and we are told to applaud the return of a coin.

II. Advertisements in Circumnavigated Analysis: What You See Is (Not) What “Facts” Lead You to Believe

A. Advertisement 1: Targeting Consumers from the “Underprivileged” World… And So Much More

After re-watching all the three ads and especially ad-1, I went on to cross-check the ad’s claim with the Piramal Finance (PFL) webpage as on 23 February 2026.

I was perplexed.

What I found was a labyrinth of mandatory “document” submissions that shattered the ad’s airy rhetoric of “kagaz se zyada neeyat”. The official site laid out, in exhaustive detail, the full documentation regime for home loans up to ₹2 crore at interest rates beginning at 9.99% p.a.:

- Full KYC (Aadhaar card, PAN card, passport, voter ID, driving licence, ration card);

- Salaried applicants: salary slips for the last 3 months, Form 16 for 2 years, bank statements evidencing salary credits for 6 months;

- Self-employed applicants: Income Tax Returns for 3 years, audited Profit & Loss statements, balance sheets, bank statements;

- Property documentation: title deeds, approved building plans, sale agreements, occupancy certificate, encumbrance certificate, valuation report, OSV stamping;

- Mandatory co-applicant in most cases;

- Credit bureau verification (CIBIL pull);

- Physical or video-based property inspection;

- Video KYC, digital signatures, and direct digital bank-statement retrieval.

The process itself was step-by-step: apply online or at a branch, expert verification of KYC/income/eligibility, credit and property review leading to a Sanction Letter, followed by disbursement. Eligibility demanded minimum age 21–23 to 60–70, both salaried and self-employed, and crucially a “good credit score”.

Every single element remained document-intensive, risk-assessed, and bound by RBI KYC Master Directions, the Prevention of Money Laundering Act (PMLA), and the Fair Practices Code.

Thus, no regulated housing finance company can legally disburse even one rupee on the basis of “neeyat” alone. The webpage exposed the ad for what it was: a linguistic fork. Ad 1 proclaims “kagaz se zyaada neeyat” (we look at intent more than papers), while the campaign’s other ad-films chant “kagaz nahin”. This is not inconsistency; it is cunning corporatism — two complementary deceptions designed to trap the same prey. One elevates moral intent above paperwork to seduce the undocumented; the other pretends paperwork has vanished entirely. Both keep the full documentary cage intact while selling the illusion of freedom.

This linguistic manoeuvre marks a peculiar, predatory switch from the visible tyrannies of print capitalism to the invisible, all-encompassing extraction of electronic/digital/cyber capitalism. Print capitalism once forged imagined communities and state legibility through physical documents — passports, ration cards, salary slips — that rendered bodies countable, taxable, and excludable. In India, that regime echoed colonial pass laws and postcolonial tools in BJP’s India like NRC/CAA, NPR, SIR, and DPDPA, where absence of paper meant erasure.

I non-chalantly ask: “Who’s got the paper, who’s got the match?”

PFL’s campaign evangelises a rupture: “kagaz se zyaada” or “kagaz nahin” — a feigned liberation from print capitalism’s bureaucratic yoke. Yet this is the duping pivot. Physical sheets dissolve, but control intensifies through data commodification.

Two arguments could be brought forth in this context.

The “Double Dealer” Argument (The Marketing Gap)

- Literal vs. Figurative: Ads wield “Kagaz Nahi” literally for attention, yet applicants face PDFs galore—it feels dishonest. No loan without documentation; just digital versions.

- Regulatory Reality: RBI’s KYC and PMLA mandate “papers”; advertising “No Papers” treads a thin line between creativity and misleading.

The “Fair Dealer” Argument (The Intent)

- Inclusion: For street vendors or contractors sans official slips, it’s a “huge relief”—sending officers to count shop footfall estimates income.

- Digitization: Heavy investment in “paperless” workflow (no physical files), even if data is required.

PFL Is Duping Through Aggressive Linguistic Marketing

I could again say that Piramal practices “Aggressive Linguistic Marketing,” redefining “paper” to suit branding: To them, paper = physical sheets; to us paupers, paper = proof required. Since they demand the information, it’s the same as other banks, wrapped in attractive candy. And this “convenience” costs more: Piramal’s rates are 2-3% higher than majors.

As a tool, I feel that surveillance capitalism arrives right here without any lame excuse: the informal borrower’s every transaction, geolocation, repayment micro-history, and “neeyat” signal becomes behavioural surplus, unilaterally claimed, analysed, and monetised by PFL’s algorithms. Derrida’s archive fever (will-to-hide) is not metaphorical here — it is the profit model. The borrower’s digital footprint is archived with feverish intensity, scored, profiled, and sold onward to credit bureaus, insurers, marketers, or state apparatuses. The India Stack (Aadhaar, UPI, Account Aggregator) supplies the infrastructure; PFL harvests the data. “Neeyat” is not trusted — it is data-mined. This is Baudrillardian hyperreal in action: the sign (“no papers / more than papers”) floats free from operational reality, preceding and superseding it. Pseudology in its purest corporate form.

The price tag reveals the predation. As of February 2026, PFL home-loan rates start at 9.99% p.a. and routinely climb to 11–12% effective for the very “informal” segment the ads romanticise. Compare with public-sector and major private banks:

- State Bank of India: ~7.25–8.70% p.a.

- Bank of Baroda: ~7.20–9.25% p.a.

- HDFC Bank: ~7.75% onwards

- ICICI Bank: ~7.45% onwards

On a ₹50 lakh loan over 30 years, the 2–3% differential adds ₹20–25 lakh or more in extra interest paid by the borrower. Processing fees reach up to 0.5–1% (often higher in practice) plus ₹2,000–5,000 appraisal charges — far above public-sector caps. The informal-sector borrower, the blacksmith, the cycle vendor, the daily-wage labourer, pays a punitive premium precisely because PFL courts the “risky” profile the ad calls virtuous.

The covert motive is accumulation of mortgaged property of the defaulter. The strategy is clinical: originate high-cost loans to the “imperfect”, trigger default, then perfect the asset through legal possession. India’s lender-friendly regime supplies the arsenal. Under the SARFAESI Act 2002, once a loan is classified NPA (90+ days), PFL issues a 60-day notice under Section 13(2), effects symbolic possession via newspaper affixation, and invokes Section 14 for Magistrate-assisted physical takeover — no court decree required in most cases. The Transfer of Property Act and Debt Recovery Tribunal provide additional teeth. PFL’s website routinely lists possessed assets; possession notices appear across states.

Let me take a textbook example for this: Siddharth Bansilal Jaju. He had taken a home loan from DHFL. After Piramal’s questionable acquisition of DHFL, the account was transferred. Without proper notice, Piramal seized his two row houses in Aurangabad. The Debt Recovery Tribunal, Aurangabad, ordered restoration on 13 May 2022. Piramal ignored the order. Jaju went public in a June 2022 press conference, alleging interest rates had been inflated to approximately 17% (against mainstream banks’ ~7%), complained to RBI and the National Housing Bank, and demanded cancellation of Piramal’s licence. The mechanics were laid bare: originate at high cost to vulnerable borrowers, engineer NPA status, seize under SARFAESI, auction at profit. This is India’s sub-prime crisis mirror — not securitised and offloaded as in 2008 America, but retained and perfected.

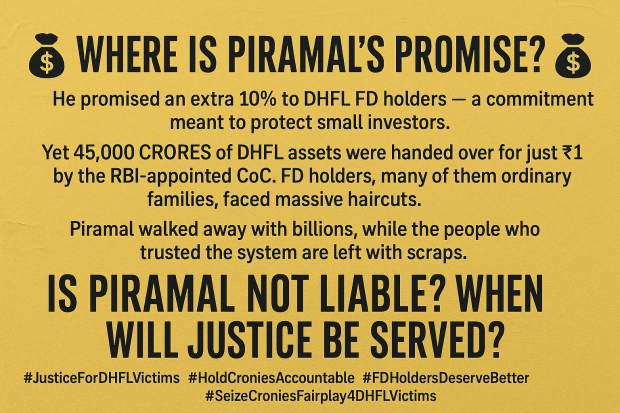

The DHFL acquisition itself appears to be the ultimate adverse possession: while multiple avoidance applications involving ₹45k crore in allegedly fraudulent, preferential, undervalued and extortionate transactions remained fully sub judice before the NCLT (with parallel appeals by promoters and victim groups still pending across NCLAT and the Supreme Court), Piramal Capital & Housing Finance executed its takeover in September 2021 and proclaimed ownership, disregarding the ongoing adjudication of title, claims and recoveries. The approved resolution plan assigned a mere notional value of Re 1 to these colossal recoverable assets, thereby extinguishing the creditors’ proprietary interest in the potential upside and vesting it exclusively in the acquirer. Retail fixed-deposit and NCD holders — predominantly elderly and middle-class savers numbering around 2.5 lakh — were simultaneously forced to absorb savage 55–77% haircuts on their lifetime savings, recovering only 23–45% of admitted claims. This sequence, as repeatedly characterised by DHFL victims in public petitions, open letters and civil discourse, constitutes a textbook instance of tortious wrong under Indian law: the tort of conversion (wrongful dominion over another’s chattels and choses in action), the tort of unjust enrichment (profiting at the direct expense of defrauded depositors), and the tort of wrongful interference with sub judice rights (premature hostile occupation of assets whose legal status was still under judicial determination).

Loaning imperfect, possessing perfect — Piramal’s real, unadvertised motto.

₹45,000 crore for Re 1 — and integrity is measured in pocket change.

The Risky Borrower as Prey: PFL’s Strategy of Loaning to the “Imperfect” for Possessive Perfection

Piramal Finance openly courts the vulnerable unorganised informal sector — the dispossessed other 98% — daily-wage labourers, street vendors, small roadside artisans, cycle-rickshaw pullers, and cash-dependent micro-entrepreneurs whose credit scores hover as low as 650 and whose earnings rarely leave a paper trail. These are precisely the figures the “Neeyat” campaign spotlights in Ad 1: the nervous blacksmith who confesses he has no “solid papers of earning,” yet is reassured by the executive that his history of repaying even one rupee proves sufficient “neeyat” for a loan. The advertisement frames this encounter as compassionate inclusion — the lender that sees character where others see only absence. In reality, it is the instantiation of Piramal’s unadvertised operating principle: Buy Imperfect, Sell Perfect.

The informal borrower enters the frame already compelled — forced by the structural failure of state schemes like PMAY (to be discussed soon) to deliver timely, affordable housing credit to the very EWS/LIG demographic it targets, by bureaucratic documentation walls that exclude those without formal slips or ITRs, and by the sheer urgency of shelter in a country where urban migration and precarious livelihoods leave no room for delay. When public banks turn them away or take months to process, when informal moneylenders charge 40–50%, the Piramal executive’s invitation — “Aaiye baat karte hain” — becomes less an offer than the only visible door left ajar. The blacksmith, the cycle vendor, the daily-wage earner are not voluntary customers; they are structurally compelled entrants into Piramal’s retail pipeline.

Once inside, the economics reveal the predation. PFL’s retail book (housing loans and loan-against-property forming the core of its growth portfolio) commands yields of around 14.4% with net interest margins of 6.3% — premiums extracted precisely from the “imperfect” profiles traditional banks shun: informal earners, small traders, households with volatile cash flows. As of Q3 FY26 (December 2025), consolidated AUM reached ₹96,690 crore (up 23% YoY), with growth business (95% of total) at ₹91,460 crore fuelling the surge; borrowings stood at approximately ₹71,678–75,532 crore against a consolidated net worth of ₹27,872 crore, placing the debt-to-equity ratio at roughly 2.7× (standalone ~2.68; debt-to-assets ~0.71), while GNPA was reported at 2.6%. A substantial portion of this debt is market-linked — secured listed NCDs, institutional borrowings, and external funding lines — underscoring a wholesale-funded architecture reliant on perpetual refinancing. The broader group balance sheet adds further strain: the pharma arm carries additional net debt of roughly ₹4,000 crore, with recent quarterly losses and weak interest coverage exposing stress beneath the surface stability. Combined group debt thus hovers around ₹75,000+ crore.

This is not a conservative balance sheet; it is a leveraged refinancing engine dependent on uninterrupted borrower cash flows to honour its own creditors.

And here lies the structural contradiction: why should economically vulnerable populations take on high-cost debt from a financial conglomerate that is itself deeply indebted? An NBFC operating at ~2.7× leverage survives on capital market confidence, bond investor appetite, and continuous repayment streams. In such a configuration, the borrower is not merely a customer; the borrower becomes the stabilising instrument of the lender’s leverage — the household EMI quietly servicing upstream NCD holders, banks, and institutional financiers. High yields are not incidental; they are necessary to sustain the cost of funds and preserve margins in a leveraged structure.

Every marginal default — inevitable when double-digit lending rates meet irregular incomes — becomes not just an individual distress event but a potential disruption in the lender’s debt-servicing chain. The response is therefore mechanised and unforgiving: 90+ days of missed EMI triggers the 60-day notice, symbolic possession via newspaper publication, Magistrate-assisted physical takeover under Section 14 of SARFAESI, and eventual auction. Possession notices and auctions persist; Gujarat cases involving defaults as low as ₹24 lakh were documented in February 2026 alone.

The asymmetry is systemic. If the borrower defaults, the house is seized. If the lender’s leverage strategy tightens under market pressure, it negotiates refinancing, raises fresh capital, taps development finance institutions, or restructures liabilities with political/crony aid. One side faces dispossession; the other faces repricing.

Risk travels downward; protection travels upward. What is described as “financial inclusion” thus begins to resemble calibrated risk redistribution — from a leveraged corporate balance sheet to the rooftops of those least capable of absorbing shock, effectively asking precarious households to underwrite the stability of a debt-laden financial conglomerate.

Through securitisation via RMBS trusts (rated AAA by agencies), PFL offloads much of the credit risk to investors while retaining servicing rights and — crucially — the full upside on foreclosed properties. The nervous blacksmith or smiling cycle vendor of the advertisement is therefore never a beneficiary of genuine financial inclusion. He is raw inventory in a deliberate originate-to-possess pipeline: loaned to while imperfect (low score, informal income, high perceived risk), then — when default arrives — possessed perfectly (the mortgaged house or plot acquired at undervalued auction prices, cleaned of encumbrances, and resold or held for capital appreciation).

This strategy mirrors, in microcosm, the macro manoeuvre of the DHFL acquisition: buy imperfect (distressed, fraud-tainted NBFC), possess perfect (rebranded empire built on the ruins of retail depositors’ savings). The campaign’s slogan of trusting “neeyat” over “kagaz” is the velvet glove concealing the iron fist of possessive perfection. The informal sector, already excluded and compelled, is not being empowered; it is being harvested — one high-cost loan, one inevitable default, one SARFAESI notice at a time.

Distrust the Shiny Ratings of Piramal Finance: Manufactured Shields for Systemic Expropriation

Piramal Finance: CRISIL AA+/Stable (assigned January 2026), ICRA/CARE AA/Stable — these are not independent verdicts but issuer-paid illusions. The same agencies that maintained DHFL at AAA while ₹31,000+ crore were diverted now underwrite Piramal’s ₹75,532 crore debt mountain. The issuer-pays model guarantees optimism bias and conflicts of interest. Ratings enabled the Re 1 DHFL heist; they now shield the high-interest predation on the very classes the ads romanticise. Governance risks, legacy DHFL forensic issues, related-party transactions, and political proximity (Piramal’s ₹85-98+ crore in electoral-bond donations to BJP and 25 crores in dubiously opaque PM CARES) are airbrushed as “non-material”.

Advertising as Normative Deflection

Hence, the entire “kagaz se zyada neeyat” performance — the blacksmith’s relieved sigh, the shopkeeper’s theatrical return of Re 1, the guard’s honest sprint after a snack packet — functions as industrial-scale normative whitewashing. While 60-second reels stage micro-morality, the parent entity stands accused of macro-dispossession on a scale that dwarfs any returned rupee. The emotional vignettes wash clean the memory of ₹50,000+ crore in vanished retail deposits, the 2.6 lakh fake PMAY accounts created by DHFL to siphon ₹1,880 crore in subsidies, and the ongoing SARFAESI drive against borrowers like Siddharth Bansilal Jaju. Corporate conscience is outsourced or offloaded to YouTube while structural expropriation proceeds uninterrupted.

Piramal’s Finance’s Loan Business’ Triumph ⊃ Failure of PMAY?

If someone is still asking for loans from Piramal, it entails the spectacular, documented failure of the BJP’s much-advertised Pradhan Mantri Awas Yojana (PMAY). As of February 2026, PMAY-U 2.0 claims 1.22 crore houses sanctioned and ~1 crore completed or under construction. Yet daily-wage earners, the precise demographic targeted by PFL’s ads, still queue at Piramal branches paying 9.99%+ because PMAY remains crippled by the very documentation barriers the campaign pretends to dissolve — plus rampant corruption. CAG audits, ED/CBI probes, and state vigilance reports reveal systemic scams:

- Nationwide: 40–45% fake beneficiaries (ineligible pucca-house owners, dead persons, politicians’ kin).

- Uttar Pradesh: ₹86 lakh cyber fraud; 9,000 fake beneficiaries in Prayagraj alone (August 2025) claiming ₹1.2 lakh each while owning double-storey houses; 338 duplicate applications across 44 districts (September 2025).

- West Bengal: 3 lakh ineligible entries, 40% deletions after verification, TMC-linked multi-storied homes on lists.

- Maharashtra: ₹1,000 crore scam via fake allotments.

- Gujarat: ₹1.85 crore cheated from 100+ women.

- DHFL itself: 2.6 lakh fictitious PMAY accounts, ₹1,880 crore subsidies fraudulently claimed.

- Haryana, Odisha, Madhya Pradesh: incomplete projects, funds diverted to imposters, political patronage.

Utilization in some pockets fell as low as 21%. Months-long bureaucratic delays, regional disparities, and outright political diversion have turned PMAY into a patronage machine rather than a housing solution. When the state’s flagship scheme fails the EWS/LIG daily-wage labourers it was built for, they are driven straight into Piramal’s 11–12% embrace — and into the jaws of SARFAESI. The ad’s benevolent executive is not filling a market gap; he is harvesting the policy failure engineered by the same regime that floods every billboard with PMAY success stories.

Thus the entire campaign — whether “kagaz se zyaada” or “kagaz nahin” — is not mere marketing. It is ideological preparation for dispossession dressed as inclusion. The underprivileged are not empowered; they are digitally documented, behaviourally profiled, loaned at punitive cost, and, when necessary, legally evicted so that Piramal’s balance sheet may move from imperfect to perfect. The Re 1 moral theatre is not coincidence; it is the miniature that conceals the macro crime.

The Arithmetic of Moral Equivalence

That single word “or” uttered by the Piramal executive — “whether you took one lakh rupees or even one rupee, you have always repaid it” — functions as an inclusive disjunction (p ∨ q). It does not exclude one amount in favour of the other; it affirms that repayment at either scale, or both simultaneously, constitutes identical proof of moral constancy. The logical embrace is total: the borrower’s character is declared invariant across magnitudes. In that open ∨ the advertisement enacts its core operation — quantitative difference collapses into qualitative sameness. ₹1 = ₹1,00,000. Not in the realm of economic value, but in the realm of moral value. The claim is absolute: if discipline exists at the micro-level, it scales indefinitely. Yet every borrower knows the opposite is true. A roadside transaction of one rupee carries negligible risk; a housing loan stretches across decades, interest compounding, foreclosure mechanisms waiting, regulatory oversight looming. The campaign bridges this unbridgeable gap not by reasoned argument but by pure emotional transference. The smallest unit is elevated into a universal moral constant.

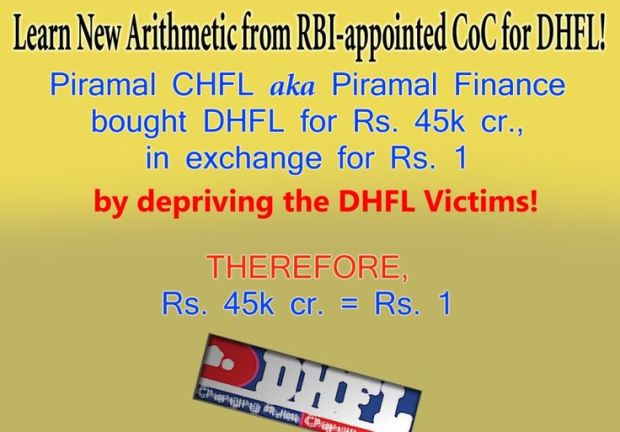

Re 1 = ₹45,000 Crore: The Founding Arithmetic Behind the Moral Campaign

The campaign’s obsessive return to the single rupee ceases to be innocent symbolism when set against Piramal’s corporate genesis. Between 2019 and 2021, DHFL collapsed under over ₹91,000 crore of debt amid documented allegations of massive fund diversion. More than 55,000 fixed-deposit holders — largely retirees, widows, and middle-class families — along with NCD investors, saw their life savings nearly wiped out.

In June 2021, the NCLT approved Piramal’s resolution plan for roughly ₹34,250–37,250 crore. Its decisive manoeuvre was this: avoidance transactions — preferential, undervalued, and fraudulent, under IBC Sections 43, 45, 50, and 66 — conservatively valued at ₹45,000 crore were assigned a notional value of exactly Re 1 and transferred in full to Piramal as the Successful Resolution Applicant.

In January 2022, the NCLAT recorded “material irregularities” and “illegalities,” directing that recoveries flow back to the benefit of all the creditors. Yet on 1 April 2025, the Supreme Court upheld the plan in full, sanctifying the “commercial wisdom of the CoC” and ruling that Section 66 recoveries belong exclusively to the SRA. Finally, on 5 February 2026, the Mumbai PMLA Special Court discharged DHFL/Piramal Finance from ₹5,050 crore money-laundering proceedings, invoking the IBC’s “clean slate” (Section 32A) immunity.

The result is textbook primitive accumulation rendered perfectly legal: systematic dispossession of small savers followed by full state-granted absolution. The company reverse-merged, shed its deposit-taking licence, rebranded as Piramal Finance, secured CRISIL AA+ ratings in January 2026, and immediately began preaching micro-honesty to the precise demographic whose savings had first capitalised its balance-sheet expansion. The psycho-linguistic arithmetic is merciless:

Re 1 returned (advertising screen) ÷ ₹45,000 crore kept (legal reality) = infinite hypocrisy multiplier.

Hypocrisy ki bhi seema hoti hai!

The Semiotic Collision: Screen Arithmetic vs. Structural Arithmetic

Inside this historical frame the advertisements’ fixation on Re 1 loses all claim to neutral symbolism. On-screen arithmetic reads: Re 1 returned = proof of integrity. Structural arithmetic reads: avoidance recoveries worth ~₹45,000 crore transferred for Re 1 under Piramal’s resolution plan. The numerical coincidence is not accidental; it is jarring precisely because the two rupees inhabit radically different moral universes. The campaign stages the voluntary surrender of negligible surplus as ethical proof. The insolvency framework stages the legal acquisition of enormous avoidance claims at a token valuation. The juxtaposition produces what can only be called founding arithmetic dissonance. The equation quietly embedded in every frame — small return equals big trust — collides head-on with an origin story in which an immense notional value is legally consolidated through the same symbolic denomination.

Primitive Accumulation and Juridical Legitimacy

The DHFL resolution is best read as accumulation by dispossession through the “original sin” of primitive accumulation: the transfer of distressed or deliberately devalued assets into consolidated capital structures under fully state-sanctioned legal frameworks. Within the IBC architecture large haircuts (routinely 55–80% across landmark cases such as Essar Steel, Bhushan Power, Videocon and DHFL) are borne overwhelmingly by the original creditors. Section 32A grants the successful resolution applicant complete immunity from prior offences, delivering the “clean slate” that allows the acquirer to emerge pristine. The judiciary, time after time, defers to the “commercial wisdom” of the Committee of Creditors. The political-economy sequence is crystalline: Crisis → Insolvency resolution → Transfer of assets → Legal absolution → Re-capitalisation. The February 2026 PMLA discharge merely seals the arc. The legal narrative ends not in liability but in institutional rehabilitation and upgraded credit ratings.

They priced ₹45,000 crore at Re 1 — and called it resolution.

Advertising After Accumulation (Post-facto)

It is only after this completed cycle of accumulation that the advertisements appear. A lender whose very expansion is structurally tethered to one of the largest insolvency acquisitions in Indian history now positions itself as the tender recogniser of everyday honesty. The target demographic — small traders, informal earners, middle-class aspirants — overlaps almost perfectly with the retail investors and fixed-deposit holders who absorbed DHFL’s losses. The symbolic tension is not incidental; it is structural. The narrative therefore acquires a darker register:

Re 1 returned (advertising screen) ÷ ₹45,000 crore consolidated (legal structure) = a permanent disjunction between moral spectacle and political economy.

The advertisements preach micro-honesty; the corporate origin story enacts macro-legal consolidation.

Let me move on from here. Let me go to the “big picture” of political economy. How does one equate Rs. 10 with a bottle of water — how does one standardise value, dignity, survival into such neat transactional metaphors by making unequal entities equal through an “=” signification? Marx supplies the decisive answer.

In the Grundrisse (1857–58) and Capital Volume 1 (1867) Marx demonstrates that the equation is never a simple arithmetic identity; capital is a social relation mediated by exchange-value and rooted in abstract human labour. Commodities possess a dual nature: use-value (the bottle quenches thirst) and exchange-value (the imposed/stipulated quantitative proportion in which it exchanges with all other commodities, expressed in money-form). Money seemingly functions as the universal equivalent, the form in which every product of labour can be equated. The price of Rs. 10 is the monetary expression of a bottle’s value, determined by socially necessary labour — the average labour required under prevailing social conditions of production. This value is not arbitrary; it is the socially validated measure that enables commodities to be equated in exchange. The bottle’s exchange-value is regulated by this quantum of average social labour, and price expresses it in money.

Marx’s theory of surplus-value adds the decisive layer: surplus-value is the excess produced by living labour beyond what is required to reproduce labour-power (wages). It arises because the capitalist purchases labour-power (labour as commodity) in return of wages. The rate of surplus-value (s/v) is surplus labour divided by necessary labour — or surplus-value divided by variable capital. On the surface, this surplus appears in mystified forms — profit, interest, and rent — not as separate sources of value but as divisions of the same mass of labour appropriated by different fractions of capital-relations.

Now consider a Piramal Finance home loan at 9.99%+ p.a. The borrower — often from the informal sector, blocked by PMAY failures and documentation walls — pays interest that exceeds mere reproduction needs. This interest is not a neutral “cost of capital” but surplus-value captured through credit. Money-capital (M) is advanced against a promise of repayment and returns as M′ — more money — the difference realised as profit/interest: M–C–M′ in financialised form. The borrower’s labour (or future labour-power) must generate enough surplus to cover both subsistence and debt service. High effective rates (11–12% for informal profiles) and SARFAESI-backed enforcement ensure that even marginal default feeds the originate-to-possess pipeline, where the home itself becomes the lender’s secured asset. The interest paid by precarious workers is thus surplus-value transferred upward through the credit system, rooted in the same exploitation dynamic Marx identified.

Contrast this with socially necessary labour performed for those unable to labour — infants, elders, the disabled. In a truly social economy, such care is necessary for the reproduction of society and future labour-power; under capitalism, it remains largely marginalized unless commodified. Marx’s framework reveals the violence here: while surplus is extracted from vulnerable borrowers through high-cost debt, the socially necessary labour of care — disproportionately performed by women and the poor — lies outside valorisation circuits or is valued only when marketised. The high-cost loan therefore forces the reproduction of the dispossessed to subsidise finance capital, converting socially necessary survival and care labour into financialised surplus. The Rs. 10 bottle reflects socially necessary labour embodied in a commodity; the loan reflects a claim on future labour enforced through interest — both governed by the same logic: living labour creates value, but surplus is privately appropriated.

Therefore, broadly speaking, the given equation materialises inside the circuits of capital. In the simple commodity circuit C–M–C′ the bottle (C) is sold for money (M) only to purchase another commodity (C′). In the capitalist circuit M–C–M′ money is advanced to buy commodities (including labour-power) in order to sell them again for more money (M′), the difference being surplus-value. Marx traces the historical genesis of the money-form through successive stages: simple equivalence (x of commodity A = y of commodity B), expanded equivalence (x A = y B or z C …), general equivalence (all commodities express their value in one privileged commodity), and finally the money-form (all commodities express their value in gold, silver or, today, fiat rupees). In Capital Chapter 1, Section 3, money appears as the “form of appearance” of value, resolving the hieroglyphical riddle of commensurability: commodities become equatable because they are all objectified abstract labour.

For Rs. 10 truly to equal one bottle, four necessary conditions must obtain. First, the bottle must exist in commodity form — the product of human labour destined for exchange, not mere personal use. Second, its production must occur under socially necessary labour: average societal conditions of technology and skill; if average labour produces one bottle, then Rs. 10 must represent exactly that quantum of social labour. Third, a functioning universal equivalent must exist — society must accept that Rs. 10 commands the same average effort tomorrow as today. Fourth, the exchange must be realised in circulation; potential value becomes actual value only when the bottle is sold and the rupees paid. Beyond these, sufficient conditions complete the picture: market equilibrium in which supply and demand balance at Rs. 10 without monopoly distortions; the full capitalist mode in which production is driven by the imperative M–C–M′ and surplus-value is extracted from wage-labour; and social validation through which the relation reproduces itself daily — workers accept wages, consumers accept prices — while fetishism renders the entire process appear natural and eternal.

Solow, in his 1956 growth model (the Solow-Swan framework), offers a contrasting yet complementary lens from the neoclassical tradition. Where Marx roots equivalence in abstract labour and class antagonism, Solow grounds it in aggregate production, marginal productivity and long-run equilibrium. Prices such as Rs. 10 emerge when every factor — capital, labour, technology — is combined so that marginal cost equals marginal revenue under perfect competition. The production function (typically Cobb-Douglas Y = A K^α L^(1-α)) yields output whose price reflects the marginal contributions of each input once the economy reaches steady state.

Solow’s necessary conditions for the equation to hold sustainably are rigorous. Constant returns to scale must prevail: doubling all inputs must exactly double output, allowing scalable production without efficiency loss. Diminishing marginal returns to capital and labour individually must operate, preventing runaway growth or collapse and enabling the steady-state condition s f(k) = (n + δ) k where investment exactly offsets depreciation and population growth. Exogenous technological progress (A growing at rate g) must continue, raising productivity and keeping real prices stable. Full employment and perfect competition must reign: labour markets clear, firms are price-takers, and P = MC = MR, so that wages equal the marginal product of labour and rents equal the marginal product of capital. Sufficient conditions then lock the system into self-reinforcing expansion: the golden-rule savings rate s = α maximises steady-state consumption per capita; initial capital stock converges to the steady-state k* through transitional dynamics; conditional convergence aligns prices across similar economies; no externalities distort true costs; and population growth and depreciation rates remain stable.

Marx and Solow therefore converge on one surface phenomenon — the apparent naturalness of Rs. 10 for a bottle — yet diverge at the root. Marx reveals the hidden labour, the exploitation, the fetishism; Solow reveals the balanced, harmonious expansion under marginal productivity and technological progress. The advertisement’s inclusive “or” borrows the authority of both while corrupting each. It treats the borrower’s tiniest repayment as the socially necessary moral unit that can be scaled indefinitely, as though micro-honesty were abstract labour and the loan were simple commodity circulation. It pretends the informal worker’s daily discipline already satisfies Solow’s constant-returns and steady-state conditions, so that character compounds smoothly into creditworthiness. Yet once the loan is disbursed, the same inclusive disjunction flips into asymmetry. The small act was never collateral; it was bait. When default arrives, SARFAESI seizes the house without regard for the moral micro-unit that was so lavishly praised.

The first advertisement does not merely position Piramal Finance as accessible; it constructs a moral counter-banking mythology. Its message is rhetorically insistent: Piramal is the empathetic disruptor that privileges character over bureaucracy, the lender that recognizes integrity where traditional institutions see deficiency, the financial interlocutor for India’s vast informal economy historically marginalized by documentary regimes.

This is not subtle branding. It is aggressive linguistic engineering—obsessive in repetition, emotionally compressed, and arithmetically fixated on a single unit: Re 1. The number functions less as currency and more as a moral calibration device. Through reiteration (“whether one lakh or even one rupee”), quantitative difference collapses into forced ethical equivalence. The smallest denomination becomes the highest ethical denomination.

The ad thereby converts arithmetic into anthropology.

Re 1 on screen, ₹45,000 crore off ledger.

Thus the campaign does not merely equate rupees. It standardises dignity and survival into the same infinitesimal token that once allowed Piramal to acquire ₹45,000 crore of avoidance value for Re 1. The “or” that sounded like empathy was always the sound of value being flattened, labour being concealed, and dispossession being dressed as inclusion. In the end, Re 1 returned on screen and Re 1 paid for ₹45,000 crore in assets are not two different rupees. They are the same symbolic coin — one side moral spectacle, the other side legal consolidation — minted by the same hand.

Having watched the blacksmith’s loan approval dissolve into regulatory reality, I move to the campaign’s signature piece, the second advertisement in our previously provided list — the one that turns a single returned rupee into the ultimate moral credential.

B. Advertisement 2: ₹499 / ₹500 Exchange — “Neeyat Sahi, Par Kagaaz Nahin….”

I sift through ads, as I shift to ad 2. I differ, and defer, at the same time.

Ad-2 could be called as the signature piece of the entire “Neeyat” campaign — still in heavy rotation across YouTube and digital platforms as of February 2026 — compresses the entire moral grammar into a crisp 30-second morality play.

The Shopkeeper’s Virtue

The shopkeeper is not merely a character; she is the embodied ideal of the campaign’s moral economy. Her exaggerated glow, the emphatic “Areh!”, the brotherly “Bhaisaab”, the luminous smile — every micro-gesture is calibrated to radiate unforced rectitude. This is no quiet, everyday honesty; it is virtue performed under bright lights for maximum affective impact. The humble shop setting, the modest transaction, the absence of any external compulsion — all conspire to present the shopkeeper as the archetype of the informal trader who possesses what banks supposedly lack: innate moral clarity.

From my pauper’s vantage, the performance feels to me like a deliberate appropriation. The very demographic the ad romanticises — small retailers, street-level entrepreneurs — overlaps with the class that lost everything in the DHFL collapse. Now their virtue is being rented to launder the image of the institution that profited from that collapse.

Theatrical Honesty as Economic Allegory

The entire scene functions as a compressed economic allegory. The customer offers more than is due; the shopkeeper voluntarily surrenders the surplus. In this micro-drama, surplus is not accumulated but renounced. The allegory maps neatly onto the campaign’s larger claim: the informal borrower who returns even one rupee of “extra” trust will honour larger obligations. Yet the allegory conceals its own sleight. In real economic life, surplus is rarely returned voluntarily; it is extracted through interest, fees, or — in default — through SARFAESI seizure. The ad inverts this reality: it celebrates the return of surplus while the institution it advertises specialises in the permanent retention of far larger surpluses. The shopkeeper’s theatrical honesty therefore serves as the perfect economic allegory for Piramal Finance itself — a lender that stages micro-renunciation while structurally practising macro-retention.

“Honesty Is Proven in What You Return”?!

The advertisement resurrects the old proverb “honesty is the best policy” and gives it a radical new twist: honesty is proven not in what one earns or keeps, but in what one voluntarily gives back. The ethical test shifts from accumulation to renunciation. The extra rupee becomes the visible certificate of character. Traditional banking demanded documentary proof of repayment capacity; Piramal’s narrative demands performative proof of repayment morality. The proverb, once a cautious maxim for personal conduct, is now weaponised as underwriting logic. The pauper watching this cannot help but remember: when Piramal acquired DHFL, it returned nothing — not one rupee of the alleged avoidable transactions, not one rupee of the lifetime savings that were haircut by 55–77%. Honesty, it seems, is the best policy only when the sums are small enough to be dramatised in thirty seconds.

Shakha Prashakha (Dir. Satyajit Ray: the imagery of a “good capitalist”: oxymoron!)

Satyajit Ray’s 1990 film Shakha Prashakha haunts this advertisement like a spectral counter-text. In the film, the patriarch is an industrialist of unimpeachable personal integrity — the “good capitalist” who believes ethical conduct can survive within a rotten system. Ray slowly dismantles the illusion: the sons are corrupt, the system devours integrity, and the father’s goodness becomes a tragic oxymoron. The shopkeeper in Ad 2 is the direct cinematic descendant of that patriarch — the “good capitalist” rendered in thirty seconds of digital warmth. Piramal Finance, through this ad, casts itself and its target borrowers in the same role: honest individuals operating inside a larger structure that the film proved cannot sustain such honesty. The oxymoron remains unresolved. A lender built on the legalised dispossession of lakhs cannot credibly perform the role of the good capitalist; it can only actively stage the image-making process as mere consumer society’s gimmick.

Conscious Capitalism of Piramal — Philanthro-capitalist facade?

Ajay Piramal has repeatedly spoken of “conscious capitalism” and “ethical wealth creation” in public addresses, interviews, and Piramal Foundation initiatives. The language is familiar: business must serve society, profit must be balanced with purpose, intent matters more than mere numbers. Ad 2 is the visual translation of that rhetoric. The shopkeeper’s voluntary return of the rupee is conscious capitalism (what Piramal often calls as “sewa bhaav”) in miniature — profit tempered by conscience. Yet the philanthro-capitalist facade cracks the moment it is placed against the DHFL origin story. The same voice that preaches conscious capitalism presided over a resolution in which conscious consent of retail depositors was never sought and their conscious suffering was never acknowledged. The foundation’s “good” works and the campaign’s feel-good vibes function as the same ideological supplement: they allow the conglomerate to wear the mask of the enlightened capitalist while the underlying arithmetic of accumulation by dispossession continues uninterrupted.

One rupee returned; forty-five thousand crore retained.

Linguistic Compression and Aggressive Framing

The slogan “Neeyat sahi par kuch kagaz nahin?” is a masterpiece of linguistic compression. In seven words it performs three aggressive moves: (1) it names the viewer’s structural exclusion (“kuch kagaz nahin”); (2) it reframes that exclusion as morally irrelevant (“neeyat sahi”); (3) it offers instant conversational redemption (“aaiye baat karte hain”). The interrogative form is not gentle; it is invasive. It forces the viewer to confront his own documentary deficiency and then immediately supplies the brand as a solution. The framing is aggressive because it converts a systemic barrier into a personal moral test that only Piramal can pass. The returned rupee becomes the linguistic anchor — the tiny material proof that the slogan’s promise is already being fulfilled in everyday life.

The Rupee as Moral Evidence

The single rupee is elevated from currency to moral exhibit. It is no longer money; it is evidence made visible. The customer could have kept silent; the shopkeeper could have pocketed the extra note. The voluntary return transforms a zero-sum transaction into a moral surplus. In semiotic terms, the rupee functions as index and symbol simultaneously — it points to the shopkeeper’s inner character and stands in for the larger trustworthiness the campaign wants to sell. From the pauper’s perspective, this is the cruelest inversion: the same denomination that was used to tokenise ₹45,000 crore of our avoidable recoveries is now paraded as the ultimate certificate of honesty. The rupee that was never returned to us is being used to sell the illusion that Piramal always returns what is not theirs.

Psychoanalytic Dissection of the “Re 1” Obsession: The Pivoting Section

The compulsive, almost liturgical repetition of Re 1 across the entire “Neeyat” campaign — and especially in this signature 30-second morality play — is no accidental branding device. It is a symptom. When read against the concrete history of the DHFL acquisition, the endless staging of the returned rupee reveals itself as something far deeper than marketing: it is the visible scar tissue of a corporate psyche that has never been allowed to mourn its own founding crime.

Freud would diagnose it at once as classic reaction formation — the ego’s frantic, over-determined defence in which the subject expresses the precise opposite of the repressed impulse in exaggerated form. The repressed impulse here is the industrial-scale taking: the legalised transfer of avoidance transactions valued at ₹45,000 crore for the notional price of exactly Re 1, followed by the permanent extinguishment of retail depositors’ claims through 55–77% haircuts. The exaggerated opposite is the ritualised micro-return: the shopkeeper’s luminous “Areh, Bhaisaab — 499!”, the glowing surrender of the single surplus coin. The greater the structural consolidation, the smaller and more theatrical the object that must be publicly given back. This is not conscious guilt in the ordinary sense; psychoanalysis does not require the subject to feel remorse. It only requires the symptom to keep returning — and Re 1 keeps returning, forever.

Yet the mechanism runs deeper than simple reaction formation. What we witness is the full internalisation of guilt conscience itself. After the September 2021 takeover, the corporate subject introjected the trauma of its own origin — the expropriation of more than 55,000 families, the widows selling vegetables, the pensioners who died waiting, the suicides, the broken homes — and then immediately disavowed it. The remorse energy does not disappear; it is channelled, via the advertising apparatus, into an insatiable need to overcompensate. Every returned rupee on screen is a psychic safety valve: a miniature restitution that keeps the corporate machine functioning while the Real of mass suffering is violently foreclosed. This is guilt laundering at the level of the institutional unconscious — not individual remorse, but systemic contradiction converted into brand equity.

Lacan sharpens the diagnosis to surgical precision. After the DHFL resolution, the corporate entity exists in permanent split: in the Symbolic order (NCLT approval, Supreme Court sanctification on 1 April 2025, Section 32A clean-slate immunity, RBI sanction, the February 5 2026 PMLA discharge) it is legally pristine — the Big Other has declared the crime “resolved”; in the Imaginary order (public perception, moral self-image, aspirational branding) it must appear as the champion of everyday ethics. The fracture appears where legality does not automatically produce ethical wholeness. The ₹45,000 crore avoidance claims function as the traumatic Real — the kernel that can never be symbolised inside the neoliberal legal order without dismantling the entire edifice. The repeated Re 1 in advertising functions as objet petit a — the impossible object of ethical purity around which corporate desire circulates endlessly, forever approaching yet never touching genuine restitution. In Ad 2 the shopkeeper’s theatrical return stages the fantasy of wholeness: “Neeyat sahi” becomes the fantasy screen that veils the constitutive lack. The louder the voice-over proclaims moral recognition, the more completely the Real of DHFL victims’ suffering is pushed outside the symbolic field.

The mirror metaphor is decisive here. The high-production, 4K advertisements function as a polished external prosthesis — a new reflective surface that replaces the shattered internal mirror. In Lacan’s mirror stage the infant gains a coherent image that conceals bodily fragmentation; here the corporate subject gains a coherent moral image that conceals the fragmentation of its own founding violence. The shopkeeper’s exaggerated warmth and emphatic “Areh, Bhaisaab!” become the mirror image the conglomerate wants to see: ethical, compassionate, trustworthy. What stares back from the fractured internal mirror — the widows, the retirees, the 2.5 lakh dispossessed — is foreclosed. The society of the spectacle fuses perfectly with the Lacanian imaginary: conscience itself has been externalised, commodified, and broadcast in prime time so that the internal void cannot be heard.

McLuhan’s dictum is uncannily exact: the medium is the message. The medium — emotionally manipulative digital shorts, algorithmically circulated, endlessly replayable — is itself the message of restored virtue. The slogans “Neeyat sahi par kuch kagaz nahin” and “honesty is proven in what you return, not what you keep” are not mere taglines; they are psycho-linguistic rituals of disavowal. By endlessly staging the return of what was “left” (the extra rupee, the fallen packet), the corporation magically inverts the trauma of what it itself “left” behind — the dignity, the rights, the savings, the lives of lakhs of families.

₹45,000 crore became Re 1 — and morality became marketing.

Žižek’s concept of “cynical reason” supplies the final, merciless layer: they (Piramal Finance/PCHFL) know very well what they did with the ₹45,000 crore, yet they stage the return of Re 1 anyway. The enjoyment is structural. The more the victims are silenced through ₹100 crore SLAPP suits, strategic legal harassment, and purported digital media blackout, the more loudly the advertisements must proclaim micro-honesty — because the same entity that preaches “return what is not yours” now weaponises the law to ensure that what was theirs is never returned. This is not hypocrisy in the naïve sense; it is the ideological supplement that makes continued extraction possible.

Piramal’s Conscience-less CSR Capitalism

This guilt laundering reaches its perfected form in Piramal’s loudly trumpeted CSR apparatus and philanthropic initiatives — the Piramal Foundation’s schools, hospitals, skill centres and rural development programmes — all packaged under the banner of “conscious capitalism.” Here the corporate subject performs its final, most refined ritual: returning to the exploited a microscopic fraction of what was plundered on a colossal scale. Marx and Engels exposed this mechanism with merciless clarity in the 19th century. In The Condition of the Working Class in England, Engels wrote of the bourgeoisie’s philanthropic institutions: they give back to the plundered victims “the hundredth part of what belongs to them,” wrapping their self-complacent, Pharisaic charity in the cloak of mighty benefactors while treading the downtrodden still deeper into degradation. For Piramal, the “Neeyat” campaign and the Foundation’s welfare projects are two sides of the same coin — conscience-less “conscious” capitalism that uses philanthropy as the last cry of the capitalist to the exploited worker.

The shopkeeper returns Re 1 on screen; the Foundation builds a clinic or funds a scholarship; the conglomerate keeps the ₹45,000 crore empire built on ruined lives. Welfare and philanthropy become the final ideological suture: a degrading alms that allows the system to continue extracting surplus without immediate collapse. It is not redemption; it is the last desperate attempt of capital to humanise itself in the eyes of those it has already dispossessed. The same hand that once took everything now offers a tiny, highly publicised portion back — and calls it conscience.

The operation does not remain confined to the corporate psyche. It simultaneously colonises consumer psychology on a mass scale. The campaign interpellates the very informal-sector subjects — street vendors, cycle pullers, daily-wage earners — who overlap sociologically with the DHFL victims, turning them into redeemable moral agents whose “neeyat” can be recognised by the same system that structurally excludes them. This is culture-industry 2.0: guilt laundered from above is transmuted into aspirational desire from below. Structural violence is converted into an individual ethical choice. The political economy is brutally efficient — the same capital that accumulated by dispossession now monetises its own guilt as brand equity, turning the victims’ demographic into willing participants in the next cycle of extraction.

The fractured corporate superego stands revealed in full pathological bloom: a conscience that has not been lost but deliberately externalised, commodified, and broadcast so that the internal fracture remains invisible — even to itself. The Neeyat campaign is therefore not marketing. It is the audible scream of a superego that knows it is guilty, yet can only survive by turning guilt into spectacle.

And in that spectacle the one rupee keeps returning — forever.

CBT and Behavioural Framing: Reconditioning the Public

From a cognitive-behavioural perspective, repetition creates associative learning.

Stimulus pairing:

- Re 1 → honesty

- Return → integrity

- Neeyat → loan access

Over time, viewers develop a conditioned response linking Piramal with fairness. This is classic disciplinary behavioural conditioning, not any value-neutral moral philosophy.

The campaign reprograms public cognition.

Not through argument — but through emotional rehearsal.

Oh, but listen to me, rambling on like some cracked professor in a padded room—me, the pensioner from Kolkata, who once had a tidy fixed deposit in DHFL, enough to see my days through with tea and toast, now reduced to hawking vegetables on the roadside while the Supreme Court’s April 1, 2025, sanctification echoes in my ears like a bad joke.

I tell myself, “Apply CBT, woman! Challenge those distorted thoughts!” That’s what the free clinic doctor said after the resolution plan gutted us in 2021, leaving me with a 77% haircut on my life’s savings. Cognitive Behavioral Therapy—reframe the catastrophe, they say. So I tried, didn’t I? I sought “help” from Piramal themselves, staring at those glowing “Neeyat” ads on my neighbor’s TV, the ones where the shopkeeper beams and hands back that sacred Re 1, proclaiming honesty like it’s a balm for the soul. “Neeyat sahi,” the voice-over coos, and I thought, maybe this is my CBT homework: pair the stimulus of my rage with their scripted integrity, recondition my brain to see Piramal not as the devourer of my nest egg but as the fair-handed lender who looks beyond papers to the heart.

I practiced, self-reflexively, like a deranged devotee in front of the screen. Every time the ad played—that liturgical return of the coin, the warm “Areh, Bhaisaab—499!”—I’d challenge my automatic thought: “They took ₹45,000 crore for Re 1, extinguished our claims, and now they parade micro-honesty?” Reframe it, I’d whisper: “No, this is behavioural framing for the greater good; it’s conditioning me to trust again, to link Re 1 with redemption.” Over weeks, I rehearsed emotionally, pairing my grief with their slogans. “Return what is not yours”—aha, stimulus! My response: integrity, not theft. But it failed, spectacularly, in the mirror of my own fractured mind. The more I tried to recondition, the louder the dissonance screamed: their February 5, 2026, PMLA discharge under Section 32A wiped their slate clean, but mine stays stained with suicides of fellow depositors, broken homes, the 55,000 families left in the dust. CBT from Piramal? It backfired into obsession; now every Re 1 I count in my vegetable stall triggers not fairness but fury, a conditioned response they never intended—for me, the victim, it’s Re 1 → betrayal, return → robbery, Neeyat → nightmare. The therapy collapses inward, self-reflexive and mocking: am I the deranged one for even trying to heal via the thief’s playbook?

NLP and Linguistic Reframing

Neuro-linguistic programming emphasizes reframing and anchoring.

“Neeyat sahi” is a linguistic anchor.

“Par kagaz nahin?” introduces a shared pain point.

“Aaiye baat karte hai” offers resolution.

The structure:

- Identify insecurity.

- Reframe it as moral adequacy.

- Anchor relief to brand identity.

The repetition of Re 1 functions as a symbolic anchor of fairness.

This is not psychiatry; it is persuasion architecture.

And here I am again, dissecting it like a mad linguist in my own head, after the ads colonized my nights—those 2025 campaign films, the ones spotlighting small-town doers, the street vendors like me, the cycle pullers echoing the very demographic they dispossessed. I turned to NLP next, post-CBT flop, thinking perhaps Piramal’s linguistic wizardry could reframe my derangement.

“Neeyat sahi,” I’d anchor it to my mirror, staring at my hollow eyes: identify the insecurity (my lost savings, the RBI’s 2021 supersession that handed DHFL to them on a platter), reframe it as moral adequacy (they see my intent, beyond my lack of papers now that I’m penniless), anchor relief to the brand (Piramal as resolver, “Aaiye baat karte hai” like an invitation to restitution). But oh, the self-reflexive irony bites deep—the ads’ structure mirrors my trauma: they identify the public’s pain (exclusion from formal finance), reframe it as ethical recognition (“We look beyond papers”), anchor to their identity as compassionate capitalists. For me, the victim, it reframes nothing; it anchors the Real wound tighter.

That Re 1, repeated in the shorts—the shopkeeper’s glow, the fallen packet returned—becomes my obsessive symbol, not of fairness but of the notional Re 1 they paid for avoidance claims, now theirs to pocket while we rot.

Like CBT, NLP fails too, derailing into delusion: I imagine dialing their helpline, whispering “Neeyat sahi par kuch kagaz nahin,” begging for my deposit back, only to hear the algorithmic echo of disavowal. Persuasion architecture? It’s brainwashing the masses while I, the deranged remnant of DHFL’s fallout, spiral deeper, self-aware yet trapped—the ads heal no one but the guilty, laundering their conscience as they extract anew. And so the one rupee returns in my dreams, forever, while my forty-five thousand crore lifeblood stays kept, forever.

A coin returned in advertisement; ₹45,000 crore absorbed in law.

Schizoanalysis and the Re 1 Machinery: Capitalism as Desiring-Production

In Anti-Oedipus: Capitalism and Schizophrenia, Deleuze & Guattari dismantle psychoanalysis’ fixation on guilt, repression, and the superego. Capitalism is not a repressive apparatus but a machine of flows—money flows, desire flows, debt flows, signs flow—all captured, decoded, and recoded without remorse. It does not repress desire; it harnesses and produces it. The DHFL acquisition is this machine at full throttle: a brutal deterritorialization of ₹91,000+ crore in debt and ₹45,000+ crore in avoidance claims, liquefied through the IBC insolvency process, stripping social anchors from 55,000+ depositors—retirees, widows, families like mine—and recoding that value into Piramal’s empire. No guilt, only flows.

Here I am, my fixed deposit gutted by a 77% haircut, fellow victims’ suicides still ringing in my ears, the Supreme Court’s April 1, 2025 sanctification and February 5, 2026 PMLA discharge sealing their clean slate while I rot. After CBT and NLP collapsed into deeper obsession, I turned to schizoanalysis as desperate “therapy”—mapping desiring-machines instead of healing Oedipal wounds. I told myself: chart the “Neeyat” campaign’s circuits (the 2023–2025 shorts, now 3.0, spotlighting rickshaw drivers, sugarcane vendors, Andhra bakery owners, Eastern UP mill operators—my exact dispossessed demographic—cast as heroic borrowers under “Hum Kagaz Se Zyada Neeyat Dekhte Hain”). Reframe trauma as flows, not fractures. But the exercise backfired spectacularly: mapping only wired me tighter into the delirium, self-reflexive rage peaking as the ads mock me from every billboard and screen.

The Re 1 as Reterritorialization

In the juridical abstraction of insolvency, Re 1 is the notional price tag slapped on the ₹45,000 crore haul. In the advertisements, Re 1 is the warm moral token returned with theatrical affection—the shopkeeper’s glowing “Areh, Bhaisaab—499!”, the guard handing back the fallen snack packet. This is no semiotic accident. The floating signifier deterritorialized in court is immediately reterritorialized in vernacular emotional intimacy. The same sign circulates across two regimes: legal void and spoken warmth. Classic Deleuzian coding.

Schizo-Capitalism: Thriving on Splits

Capitalism is “schizo” not because it is mentally ill, but because it produces and feeds on splits—law versus morality, accumulation versus inclusion, extraction versus empathy. Piramal embodies this perfectly. The macro-machine runs on the 2021 takeover, Section 32A immunity, AA+ ratings post-merger. The micro-machine runs on ads’ micro-honesty: the father completing his kacha-pakka home, the daughter rebuilding the nukkad bakery. These are not contradictions; they are complementary flows. Affect lubricates extraction. Capitalism requires feeling to keep the machine humming.

Phonocentric Capitalism’s Anesthetic

The campaign abandons logocentric justification—documents, balance sheets, written law—and goes phonocentric: spoken reassurance, warm vernacular address—“Bhaisaab,” “Kaka,” “Aaiye baat karte hai”—tone and voice preceding paper. Derrida’s critique is uncannily apt here: phonocentrism privileges presence over structure. The ads symbolically command: trust the voice, not the “kagaz.” Yet the entire empire rests on logocentric contracts—the very documentation that extinguished our claims. Phonocentrism anesthetizes the written violence that made it all possible.

Capitalism as Decoding Machine

Deleuze & Guattari describe capitalism as uniquely capable of decoding all traditional values, converting them into exchange flows, and reinserting them as commodities. Here, honesty becomes a brand asset, “neeyat” a marketing motif, the moral universe of small traders raw material for extraction. Capitalism does not suppress guilt; it monetizes it, turning moral anxiety into ad equity.

Capitalism is profoundly illiterate—writing has never been its thing.

It thrives not on the inscribed codes of ancient territories or the despotic overcodes of scripture and law, but on the axiomatic of decoded, abstract quantities: money as pure flow, desire as production without fixed inscription. Where previous social machines inscribed meaning on bodies and earth through ritual marks, genealogies, and territorial signs—writing as capture and overcoding—capitalism decodes these, replacing them with numerical equivalences that require no deep literacy, no hermeneutic depth. The balance sheet is not a text to be read for eternal truth; it is a transient diagram of flows to be accelerated or curtailed. The contract that extinguished our DHFL claims under Section 32A is not sacred writing but a machinic operation, a fleeting axiomatic that wipes the slate without needing narrative justification.

This illiteracy is why the “Neeyat” campaign must go phonocentric: voice, tone, warmth—“Bhaisaab,” “Aaiye baat karte hai”—become the privileged medium, privileging spoken presence over the dead letter of documents. Derrida’s phonocentrism critique finds its capitalist perversion here: the ads command trust in the living voice, the reassuring vernacular hum, precisely because capitalism has no stake in writing’s permanence or authority. Writing belongs to the old codes it has already deterritorialized; capitalism prefers the ephemeral, the oral-affective, the algorithmic signal that circulates without needing to be legible as scripture. The empire rests on logocentric legal artifacts (NCLT order, RBI sanctions, Supreme Court nods on April 1, 2025), yet it performs illiteracy in public—dismissing “kagaz” as secondary to “neeyat”—to anesthetize the violence of those very documents.

In my deranged stall-side reflections, this hits hardest: the ads decode my moral universe—the dignity of small trade, the intent behind every hard-earned rupee—and reinsert it as commodity, as brand motif for their lending machine. No guilt inscribed, no superego scar; just flows monetized. Capitalism doesn’t write its crimes; it speaks them away in warm tones, then lets the interest accrue in silence. The Re 1 returns not as written restitution but as spoken token, forever circulating in the illiterate circuits of spectacle and extraction. My savings, decoded long ago, remain kept—off the page, beyond the voice, in the pure flow where writing never mattered.

Desiring-Machines

Desire is not lack; it is (re-)production. The “Neeyat” campaign manufactures real desires—for recognition (“my neeyat matters”), for inclusion (“loan without humiliation”), for dignity—and attaches them to financial products. Capital accumulated through insolvency now feeds on the very informal earners’ yearning for moral validation it helped create. This is not hypocrisy in the moral sense; it is machinic efficiency at its most brutal.

Anti-Oedipal Rupee Flows

Freud reads Re 1 as reaction formation. Lacan reads it as objet petit a veiling lack. Deleuze & Guattari read it as circulation: a flow-unit. In court, Re 1 codes the asset transfer. In advertising, Re 1 codes ethical reassurance. The sign travels across regimes, endlessly productive.

The system is structurally elegant: accumulate via state-enabled insolvency, absorb public moral anxiety through ads, draw the same demographic back in as borrowers, resume extraction through interest flows. No fractured superego to heal—only circuits. The campaign is not confession; it is flow-management. The rupee returns on screen; interest and empire grow off-screen.

Re 1 as Capitalist Microchip

Across the three lenses: Freud’s defense mechanism, Lacan’s impossible object masking lack, Deleuze & Guattari’s desiring-machine component in reterritorialized flows. But schizoanalysis cuts deepest: there is no superego fracture to mend. Capitalism has no superego—only circuits. Guilt is not confessed; it is converted into spectacle and monetized to the public sphere.

And so my “therapy” implodes. Charting these flows did not liberate me; it plunged me deeper into the machine’s delirium. The bakery daughter on the billboard smiles at my vegetable stall, her “neeyat se badhna” a cruel taunt against my stagnation. Desire is produced, but for their gain. The rupee flows in my dreams, forever returned on screen; my savings, forever decoded and kept off-screen.

Thus the spectacle must escalate: from the fetish of the returned rupee to the choreography of returned goods — where vigilance performs virtue, and retrieval rehearses redemption.

C. Advertisement 3: The Guard’s Kindness – Vigilance as Veneer, Retrieval as Ruse