Who Pays, Who Bribes, Who Flees, Who Profits: BJP’s Swelling Coffers Amid Exploding External Debt

Who Pays, Who Bribes, Who Flees, Who Profits: BJP’s Swelling Coffers Amid Exploding External Debt

Posted on 6th January, 2026 (GMT 06:26 hrs)

ABSTRACT

India’s neoliberal delusion stands exposed in this searing critique: As the ruling Bharatiya Janata Party (BJP) amasses an astronomical financial empire—ballooning from modest pre-2014 assets to ₹7,113 crore in cash/bank balances and over ₹10,107 crore in election war chests by late 2025, propelled by ₹6,088 crore in opaque donations overwhelmingly routed through electoral trusts post the 2024 bonds ban—the nation reels under a crushing $747 billion external debt surge since 2014, an 81-82% general government debt-to-GDP ratio, and regressive taxation that fleeces salaried citizens and the poor to service crony megaprojects. This comprehensive exposé unmasks the entrenched nexus of corporate-political capture: conglomerates like Adani-Ambani reap windfalls from policy favors while enjoying 15-20% effective tax rates; super-rich wilful defaulters (2,104 owing ₹1.76 lakh crore) evade justice through sham settlements and fugitivity; flagship schemes like PMKVY and PMAY bleed billions in scams and diversions; and opacity shrouds funds like PM CARES. Amid extreme inequality (top 1% holding 40% wealth), youth despair, and looming hyper-inflation risks, the article demands radical reforms—wealth taxes, donor caps, CAG audits, GST relief on essentials—to dismantle this oligarchic plunder before systemic collapse engulfs the exploited masses.

In Continuation With

SECTION I. BJP’s Increasing Assets, Crony Oligopoly and More…

0. Introduction

In India’s neoliberal era, where GDP growth is fetishized as the ultimate measure of success while systematically masking rampant structural inequalities, a grotesque fiscal paradox unfolds—one deepened by extreme disparities in wealth, income, hunger, and poverty.

As of FY2025-26, the general government debt-to-GDP ratio remains stubbornly high at approximately 81-82%, with central government debt projected at 56.1% (down marginally from 57.1% revised in FY2024-25). Central government liabilities exceed ₹185 lakh crore (end-March 2025), driven by chronic fiscal deficits, extravagant pandemic-era borrowing, and massive infrastructure splurges that disproportionately enrich a handful of selected corporate cronies tied to the ruling establishment—delivering windfall gains to conglomerates while yielding meager broad-based returns.

Economists insist debt is “productive” only when it spurs sustainable investments and income; yet in India, debt accumulation has wildly outstripped any tangible sustainabilities, pushing the nation toward a dangerous creditor-controlled economy. Foreign lenders and domestic banks increasingly call the shots, imposing implicit conditionalities that force austerity on the masses, fuel persistent inflation, and rely on regressive taxation—all while corporates enjoy lavish exemptions, bailouts, and policy capture. Salaried workers, farmers and the informal sector bear the heaviest load, with personal income taxes surging far faster than tepid corporate contributions.

Critics warn that this unchecked debt trajectory risks hyper-inflationary spirals as this fiscal indiscipline persists—eroding purchasing power, devastating savings, and triggering currency devaluation in a worst-case scenario reminiscent of historical debt crises elsewhere.

This crony-fueled inequality escalates alongside the ruling Bharatiya Janata Party (BJP)’s meteoric financial ascent: assets and funds have ballooned dramatically, with cash and bank balances reaching ₹7,113 crore as of March 2024 and separate election-specific accounts swelling to over ₹10,107 crore by late 2025 (a 115-fold increase from ₹88 crore in 2004). Donations above ₹20,000 surged to approximately ₹6,088-6,654 crore in FY2024-25 (a 50-68% jump from ~₹3,967-4,000 crore in 2023-24), routed primarily through electoral trusts post the 2024 electoral bonds ban—capturing ~85% of total trust donations nationwide and dwarfing Congress receipts (~₹522 crore donations, total funds ~₹134-857 crore across accounts).

Invoking a Durkheimian financial anomie—where norms of fairness, proportionality, and oversight have utterly collapsed in a state of perpetual financial disequilibrium—this aligns with entrenched corporate-political nexuses in duopolies like Adani-Ambani, facilitated by deliberate institutional opacity (pre-2024 electoral bonds, PM CARES exemptions from scrutiny and so on…).

Key Indicators (2024-25/2025, Verified as of January 2026):

- Public Debt: General government ~81-82% of GDP; central ~57.1% (RE 2024-25), projected 56.1% (2025-26).

- Wealth Inequality (World Inequality Report 2026): Top 1% holds ~40% of national wealth (highest since colonial era); top 10% ~65%; bottom 50% ~6%.

- Income Inequality (World Inequality Report 2026): Top 10% captures ~58% of national income; top 1% ~22-23%; bottom 50% ~15%.

- Poverty: Multidimensional poverty ~11-15% (2022-23 estimates, varying by source: NITI Aayog ~11.3%, NFHS-5/UNDP ~15%); substantial headline reductions mask lingering vulnerability for millions.

- Hunger: Global Hunger Index 2025 score 25.8 (“serious” category), rank 102nd out of 123 countries.

- Youth Unemployment: ~10-18% (ages 15-29, national ~10.2% in 2023-24, urban up to ~19% in 2025); nearly double to triple the overall ~4.7-5.6%; urban youth ~17-19%.

- BJP Finances: Donations ~₹6,088 crore (2024-25); bank/cash ~₹6,900-7,113 crore (estimates); war chest ~₹10,107 crore (estimates).

- Adani-Ambani Wealth: Combined ~₹16-20 lakh crore ($198-235 billion, fluctuating; Mukesh Ambani ~$108-113 billion, Gautam Adani ~$66-86 billion).

- Tax Trends: Gross direct taxes ~₹25-27 lakh crore (CIT ~₹12.4 lakh crore, PIT ~₹12.9 lakh crore; PIT growth ~17-21% vs. CIT ~7-10%); GST ~₹22.08 lakh crore (full FY 2024-25).

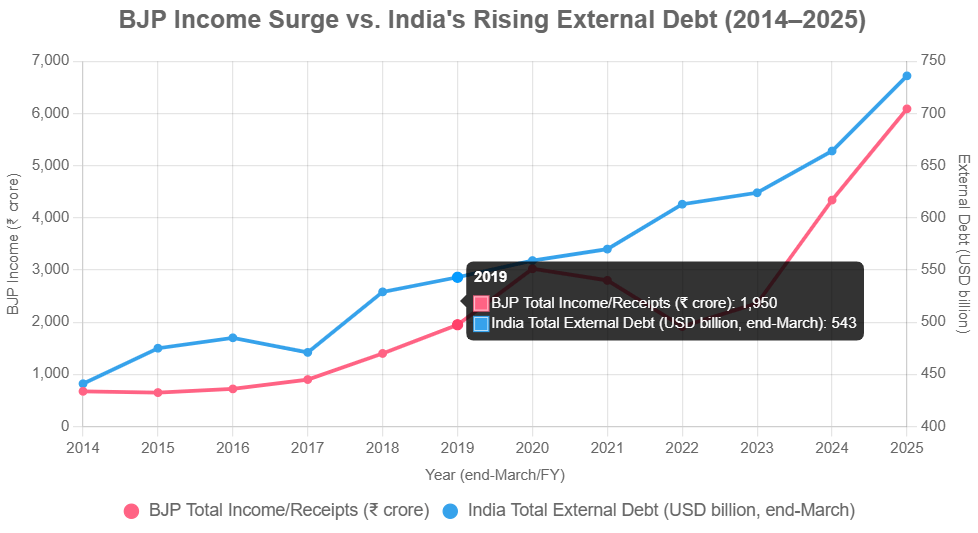

1. BJP’s Explosive Asset Growth: A Timeline of Accumulation Amidst Huge External Debt

The BJP’s financial trajectory exemplifies a predatory ascent, propelled by increasingly opaque funding channels—first electoral bonds (scrapped in 2024), now dominated by electoral trusts—that forge deep corporate alliances at the expense of public welfare and democratic equity. This unchecked accumulation has transformed the party into a financial behemoth, dwarfing rivals and entrenching a skewed electoral playing field.

This grotesque contradiction sharpens when juxtaposed against India’s soaring public external debt since 2014: total external debt has surged by over 70% from ~USD 441 billion at end-March 2014 to USD 736 billion by end-March 2025 (and further to ~USD 747 billion by June 2025), with significant portions comprising sovereign and publicly guaranteed borrowings. The ultimate liability for this external debt—serviced through taxpayer revenues, potential currency risks, and future fiscal burdens—falls squarely on the public, even as private corporates and the ruling party’s coffers swell exponentially through policy-driven windfalls and opaque donations.

Below is a verified timeline of the BJP’s declared total assets and income/receipts (primarily donations above ₹20,000, as per ECI and ADR reports), highlighting the explosive growth phases:

| Financial Year | Total Assets (₹ crore) | Total Income/Receipts (₹ crore) | Key Notes |

|---|---|---|---|

| 2013–14 | ~780 | ~674 | Pre-Modi era peak; overtaken Congress as wealthiest party. |

| 2014–15 | ~1,200 (est.) | ~650 (est.) | Initial post-victory surge. |

| 2015–16 | ~1,500 (est.) | ~720 (est.) | Steady buildup amid policy shifts. |

| 2016–17 | ~2,100 (est.) | ~900 (est.) | Demonetization period; partial disclosures. |

| 2017–18 | ~3,000 (est.) | ~1,400 (est.) | Electoral bonds introduced, marking onset of massive inflows. |

| 2018–19 | ~4,200 (est.) | ~1,950 (est.) | Bonds in full swing; receipts double prior levels. |

| 2019–20 | ~4,848 | ~2,555–3,623 | Peak bond era; assets near ₹5,000 cr amid pandemic onset. |

| 2020–21 | ~6,100 (est.) | ~2,800 (est.) | COVID-era influxes via bonds and other channels. |

| 2021–22 | ~6,800 (est.) | ~1,917 (incl. ~₹1,294 cr bonds) | Bonds ~54–67% of donations. |

| 2022–23 | ~8,100 (est.) | ~2,361 (incl. ~₹1,294 cr bonds) | Continued growth post-economic recovery. |

| 2023–24 | ~9,100+ (est.) | ~4,340 (total income); donations ~₹2,243–3,967 | Highest pre-ban bond inflows (~₹1,686 cr est.); total income 74% of all national parties. |

| 2024–25 | Cash/bank balance ~₹7,114; separate election funds ~₹10,107 | Donations ~₹6,088 (incl. ~₹3,143 cr from trusts) | Post-bond ban shift to trusts; BJP captured ~82–85% of total trust donations nationwide (~₹3,811 cr total to parties); 50%+ jump in donations, ~12x Congress (~₹522 cr). |

This dual-axis line chart illustrates the parallel trajectories: BJP receipts multiplying over 9-fold (with sharp spikes post-electoral bonds and trusts), while external debt climbs steadily—underscoring how private-political enrichment coincides with escalating public fiscal liabilities.

1.1. Observations and Trends

This order-of-magnitude expansion—from a modest ~₹780 crore in assets and ~₹674 crore in receipts pre-2014 to cash/bank balances exceeding ₹7,114 crore and separate election-specific funds surpassing ₹10,107 crore by late 2025—reveals a profound systemic capture. Corporate quid pro quo thrives through policy favors (e.g., lucrative infrastructure contracts, regulatory easing, and airport/port privatizations), entrenching political dominance, undermining democratic accountability, and entrenching crony capitalism on an unprecedented scale.

Assets, as per audited ECI submissions compiled by ADR and MyNeta.info, encompass fixed assets (party offices, vehicles), cash holdings, bank balances, fixed deposits, and advances/loans. The growth trajectory accelerated dramatically post-2018 with the introduction of electoral bonds—a scheme ruled unconstitutional and scrapped by the Supreme Court in February 2024—followed by a seamless pivot to electoral trusts, which funneled ~₹3,143 crore to the BJP in FY2024-25 alone (capturing 82-85% of nationwide trust donations totaling ~₹3,811 crore). Receipts have effectively doubled (or more) with each major election cycle, reflecting hyper-strategic, institutionalized fundraising tied to power incumbency.

Not captured in these figures: undisclosed internal funds, potential parallel economies, or “black money” channels that evade scrutiny. Recent spikes in FY2024-25 coincide with the 2024 Lok Sabha polls, state elections (including Delhi), and aggressive trust inflows from major corporates—yet full audited details for 2024-25 remain partially opaque pending complete ECI disclosures.

This private-political wealth accumulation stands in grotesque financial dissonance with India’s escalating public external debt burden, which has surged ~67% since end-March 2014 (from ~USD 440.6 billion to USD 736.3 billion by end-March 2025, further rising to USD 747.2 billion by June 2025). While much of this total external debt is private/commercial (sovereign portion ~23%, or USD 168.4 billion in 2025), the state borrows heavily to finance persistent fiscal deficits and grand infrastructure projects—many awarded to the very conglomerates (e.g., Adani, MEIL, Tata entities) that dominate BJP’s donor lists via trusts and prior bonds. These projects deliver outsized profits to select corporates, who in turn recycle gains into political funding, while the repayment risks, currency vulnerabilities, and intergenerational debt obligations are socialized onto the public through higher taxes, inflated costs, and curtailed welfare spending—exposing a vicious cycle of capitalist enrichment amid national indebtedness.

2. Laying Some Channels Bare: A Selected Analysis of Certain Sources of BJP’s Increased Assets

The BJP’s financial dominance is not merely organic growth but the outcome of engineered funding channels that have systematically funneled corporate wealth into the ruling party’s coffers while preserving donor anonymity and evading meaningful scrutiny. Two mechanisms stand out for their scale, opacity, and direct contribution to the party’s explosive asset accumulation: electoral bonds (2018–2024) and the subsequent pivot to electoral trusts (post-2024). These channels—first bonds, now trusts—operate as legalized conduits for corporate influence, transforming policy capture into political capital. The result is a self-reinforcing loop: state resources and contracts flow to select corporates, who recycle profits into ruling-party funding, entrenching a crony-political nexus while the public bears the fiscal and democratic costs. Full donor-level transparency remains elusive, as trusts disclose only bulk figures, perpetuating the very opacity the Supreme Court sought to dismantle.

This analysis also extends to related government schemes and financial practices that highlight systemic irregularities, including the Pradhan Mantri Kaushal Vikas Yojana (PMKVY), bank loan write-offs, and the Pradhan Mantri Awas Yojana (PMAY). These reveal patterns of mismanagement, fraud, and favoritism that indirectly bolster the ruling party’s ecosystem through unrecovered public funds and crony benefits.

2.1. Electoral Bonds: The Anonymous Precursor (2018-2024)

Introduced in 2018 as a purportedly transparent alternative to cash donations, electoral bonds were bearer instruments purchased from the State Bank of India (SBI) in denominations from ₹1,000 to ₹1 crore, allowing anonymous contributions to political parties via designated bank accounts. No donor disclosure was required, only aggregate reporting by parties to the Election Commission of India (ECI). Bonds had a 15-day validity window and were tax-deductible for donors, with no cap on corporate contributions after amendments to the Companies Act. Key rules included: Indian citizens/companies only (no foreigners); anonymous; no cash; encashable only by eligible parties (those with >1% vote share).

The scheme was struck down by the Supreme Court in February 2024 as unconstitutional, violating the right to information under Article 19(1)(a), and enabling quid pro quo arrangements through anonymity. Post-verdict, SBI disclosed data on purchases and encashments from April 2019 to January 2024, with full donor-recipient matching revealed.

How They Worked (Step-by-Step):

- Buyers (individuals/companies) purchased bonds from SBI branches during specified windows.

- Bonds were anonymous—no donor names linked to recipients.

- Parties encashed bonds at SBI, reporting only totals to ECI.

- Tax benefits: 100% deductible under Section 80GGB/80GGC; no 7.5% profit cap for corporates post-2017 amendments.

- Post-SC order, full donor-recipient matching disclosed.

Data and Trends: A total of 28,030 electoral bonds worth ₹16,518 crore were sold from March 2018 to January 2024. BJP encashed the lion’s share: ₹6,060.5 crore (47.5% of total), peaking at ₹2,024.75 crore in 2019-20 (82% of all bonds that year) and ₹1,294.15 crore in 2022-23 (46%). Other parties: Congress ₹1,334 crore, TMC ₹1,609 crore, etc. Bonds dominated BJP funding (38-54% of income in peak years) until the ban shifted inflows to trusts. This period directly correlates with the steepest rise in BJP assets from ~₹3,000 crore (2017–18) to over ₹9,100 crore (2023–24).

Major Donors to BJP (Revealed Post-SC Disclosure): Top contributors included infrastructure and lottery firms, often linked to contracts or regulatory favors:

- Megha Engineering & Infrastructures Ltd (MEIL): ₹966 crore total (₹584 crore to BJP).

- Qwik Supply Chain Pvt Ltd: ₹375 crore to BJP.

- Future Gaming & Hotel Services: ₹1,368 crore total (significant portion to BJP).

- Others: Vedanta, Bharti Group, MKJ Enterprises, etc., with donations >₹100 crore each to BJP. 22 companies donated >₹100 crore each overall.

Analysis: Bonds exemplified opacity, allowing unlimited anonymous corporate funding that skewed towards the ruling party (BJP received ~47-50% of all bonds). This fostered cronyism, with donors like MEIL securing massive infrastructure projects (₹15,000+ crore) post-donations. Post-ban, funding shifted to trusts, but concentration persisted.

Vs. Trusts/PM CARES: Bonds offered zero donor disclosure (unlike trusts’ mandatory reporting); similar tax perks but no RTI/CAG oversight. SC verdict emphasized transparency for fair elections.

2.2. Post-Ban Pivot: Electoral Trusts as the New Veil

Following the bonds’ scrapping, funding seamlessly shifted to electoral trusts—tax-exempt entities (under Section 80GGB/GGC) that pool corporate donations and distribute them to parties with minimal donor disclosure (only aggregate trust-level data required). These non-profit entities under Section 13B of the Income Tax Act and the 2013 CBDT Scheme were designed for transparent political funding—collecting donations from Indian citizens/companies (no foreigners or anonymous cash) and distributing to parties with full disclosure to ECI and Income Tax.

How They Work (Step-by-Step):

- Donors contribute to trusts (tax-deductible under 80GGB/80GGC).

- Trusts record and distribute 100% to parties (minimal admin costs).

- Both trusts and parties disclose in annual filings.

Key Rules: Mandatory transparency; no anonymity; audited and exempt under 13B if compliant. Major trusts: Prudent (largest), Progressive, Satya, People’s, New Democratic.

2024-25 Data: Corporate donations via nine trusts tripled to ₹3,811 crore (from ₹1,218 crore in 2023-24), with BJP cornering 82% (~₹3,143 crore). This shift propelled a 50–68% surge in declared donations for FY2024–25 (~₹6,088 crore total for BJP), pushing cash/bank balances to ₹7,114 crore and separate election war chests beyond ₹10,107 crore.

- Dominant Trust: Prudent Electoral Trust (~₹2,668 crore total inflows, ~90% routed to BJP at ~₹2,181 crore).

- Major Contributors (via Prudent and others): Megha Engineering & Infrastructures Ltd (MEIL) (~₹175 crore), Vedanta, Qwik Supply Chain (Lulu Group), Dr. Reddy’s, Hetero, Tata Group (~₹915 crore via Progressive), Jindal (~₹157 crore), DLF/Ashok Leyland (~₹100 crore each), Mahindra (~₹160 crore via New Democratic), Bharti Airtel (~₹38.8 crore), and multiple realty and infra firms—many repeat bond buyers now repurposed through trusts.

Analysis: This shift increased formal transparency but entrenched corporate concentration, raising cronyism concerns. Trusts mandate disclosure (unlike bonds’ anonymity, struck down for violating Article 19(1)(a)). Yet, they allow massive influence, with BJP dominating inflows—nearly 12 times Congress’s ₹522 crore total receipts vs. rivals.

2.3. The Recurring Donor Ecosystem

A striking pattern emerges: the same conglomerates dominating bond purchases continue to lead trust contributions, often securing massive public contracts in infrastructure (airports, highways, ports), mining, and energy sectors. Examples include:

- MEIL: Top bond buyer (₹966 crore pre-ban) → major trust donor → awarded ₹15,000+ crore projects.

- Adani Group entities: Indirect but significant via affiliates → beneficiaries of port, airport, and power deals worth trillions.

- Vedanta: Consistent donor across both regimes → favorable mining and regulatory outcomes.

- Tata Group: ₹915 crore via trusts → approvals for semiconductor units shortly after.

- Bharti Airtel, Torrent, Aurobindo Pharma: Overlaps in donations and government favors.

2.4. PM CARES Fund: Ambiguous Grey Zone of Opacity

Launched in March 2020 as a public charitable trust for emergencies (chaired by PM, with cabinet ministers), PM CARES offers 100% tax exemptions and CSR eligibility. Yet, it’s “ambiguous”: Not a government fund (despite .gov.in domain and state machinery), exempt from RTI/CAG audits, audited privately. No full donor lists; partial via media/CSR filings.

Donations Data: Voluntary contributions peaked at ₹7,184 crore in 2020-21, falling to ₹1,938 crore in 2021-22 and ₹912 crore in FY23 (total voluntary). Foreign inflows: ₹495 crore in 2020-21, ₹40 crore in 2021-22, ₹2.57 crore in 2022-23. Early years saw thousands via CSR; major reported: Reliance (~₹500 crore), Tata (~₹500 crore), Aditya Birla (~₹400 crore), Adani (~₹100 crore), PSUs like ONGC (~₹370 crore). Foreign inflows (e.g., Chinese firms like TikTok/Xiaomi) added controversy. Transparency: Limited; no full lists.

Vs. Trusts/Parties: No RTI; partial disclosure; no political use (officially), but overlaps with donors signal soft power. Courts upheld status (2020 dismissals), rejecting CAG audits or NDRF transfers.

2.5. Corporate Donations: PM CARES vs. BJP Trusts—Overlaps and Scale

Corporate funding to PM CARES (opaque, CSR-focused) vs. BJP via trusts (disclosed, political) reveals strategic duality:

- PM CARES (2020-23): ~₹912 crore in FY23 (total voluntary); early years thousands via CSR. Donors: Reliance, Tata, Adani, JSW, PSUs (60% of listed entities, ~₹2,900 crore). Transparency: Limited; no full lists.

- BJP via Trusts (2024-25): ~₹3,143 crore (82% of ₹3,811 crore total). Donors: Tata (~₹915 crore), L&T-linked (~₹500 crore), MEIL (~₹175 crore), Jindal, DLF, Vedanta, Mahindra. Transparency: High, per ECI.

Overlaps: Tata, L&T/Elevated Avenue, MEIL, Bharti/Airtel, Torrent, Aurobindo Pharma donated to both—CSR to PM CARES for “philanthropy,” trusts for direct political leverage. Network: Concentrated in conglomerates like Adani-Ambani (combined wealth ~₹30-35 lakh crore), gaining contracts/policies.

Comparative Snapshot:

| Aspect | PM CARES | BJP via Trusts |

|---|---|---|

| Recent Sums | ~₹912 crore (FY23) | ~₹3,143 crore (2024-25) |

| Donor Disclosure | Partial/opaque | Mandatory/public |

| Major Donors | Reliance, Tata, Adani, PSUs | Tata, L&T, MEIL, Jindal |

| Purpose | Emergency relief (CSR) | Political funding |

Implications: Overlaps indicate “state-corporate synergy,” where donations buy influence, exacerbating duopoly capitalism.

2.6. PMKVY: Teaching How to Do Scams—BJP-led Regime Itself Is Giving the Training

Launched in 2015, Pradhan Mantri Kaushal Vikas Yojana (PMKVY) aimed to skill India’s youth, with three phases (2015-2022) having an outlay of ~₹14,450 crore and targets to train/certify 1.32 crore candidates. A fourth phase began in 2023. A recent CAG audit (Report No. 20 of 2025) uncovered unimaginable irregularities, including fake data and fraud.

The audit revealed: Out of 95.9 lakh trainee records, bank account details were missing, blank, invalid (e.g., 11111111, 123456789), or marked “N/A” for 90.66 lakh (94%). Even among the rest, 52,000 had repeated numbers. The same email IDs and phone numbers (e.g., 11111, abc@gmail.com) were used for tens of thousands of candidates.

Further scams: A company named NMP claimed to train 33,000 people but uploaded the same photos for different batches across states (e.g., same photo for Bihar and Uttar Pradesh, zoomed/altered for Maharashtra and Rajasthan). Candidates’ profiles, testimonials, and signatures were reused. Background posters mismatched training dates/courses; people in doctors’ coats were listed for media training. Records showed 30,000 trainers in 33 gyms (~900 per gym, far exceeding reality).

Inspections were fabricated: One inspector, Ashish Sunwal, claimed to inspect centers in eight states (Andhra Pradesh to Telangana) in a single day. Similar impossibilities across Gujarat, Bihar, and Bengal.

Outcomes: Of 56.14 lakh certified under Short-Term Training/Special Projects, only 23.18 lakh (41%) were placed. In Kerala, incorrect placement documents were produced. Approximately ₹10,194 crore was released, with ₹9,261 crore utilized, but much went to ghosts. The scheme, meant to skill youth, ended up as a ₹14,450 crore lesson in looting.

2.7. Over the Last Ten Years Alone, Indian Banks Have Written Off Loans Worth More Than ₹16 Lakh Crore

From April 2014 to September 2024, Indian banks wrote off ₹16.61 lakh crore in loans, recovering only ₹2.70 lakh crore (~16%). Public sector banks accounted for ₹12.09 lakh crore in write-offs, recovering ₹2.17 lakh crore; private sector: ₹4.47 lakh crore, recovering ₹53,248 crore. Recovery rate: ~1.6% per annum.

When a loan becomes a Non-Performing Asset (NPA) and recovery fails, it’s written off to clean balance sheets—but liability remains. RBI data shows only 13-16% recovered overall. Peak write-offs: ₹2.36 lakh crore in FY19; lowest: ₹58,786 crore in FY15. FY24: ₹1.70 lakh crore (1% of outstanding credit).

Examples: Vijay Mallya’s Kingfisher Airlines took ₹9,000 crore, recovered ~₹1,000 crore. Public sector banks reported record profits (₹1.41 lakh crore in FY24), but gross NPAs fell to 2.5% by September 2024. Challenges persist in large corporate defaults; banks pursue legal actions and negotiations.

This connects to the larger financial reality: Unrecovered loans burden the public, while crony corporates (often donors) benefit from write-offs and new contracts.

2.8. PMAY Funding Flows and BJP’s Alleged Monetization Through Corruption

Launched in 2015 under the Modi-led BJP government, Pradhan Mantri Awas Yojana (PMAY) aims for “Housing for All” with two components: PMAY-Urban (PMAY-U) and PMAY-Gramin (PMAY-G). Total central assistance committed: ₹2.05 lakh crore since inception; released: ₹1.76 lakh crore as of early 2026. Funding flow: Centre provides 60-90% share (e.g., ₹1.2-2.5 lakh subsidy per house), states/ULBs contribute the rest. Disbursements occur via DBT to beneficiaries or contractors. Sanctioned houses: ~122 lakh (PMAY-U 2.0 added 1.41 lakh in 2025); completed: ~85-90 lakh. States implement, leading to vulnerabilities in beneficiary selection, tendering, and audits.

Corruption Data and Patterns: CAG audits reveal systemic irregularities, often in BJP-ruled states, totaling billions in diverted funds. Key cases (from CAG reports 2024-2025):

| State (BJP-Ruled During Period) | Irregularity Type | Amount Involved | Details/Source |

|---|---|---|---|

| Madhya Pradesh (2018-2023) | Ineligible beneficiaries, fund diversion | ₹15 crore+ | 1,555 ineligible (minors, relatives); incomplete projects. CAG Report 2024. |

| Uttar Pradesh (2017-present) | Mismanagement, ineligible allottees; cyber fraud | Hundreds of crores estimated; ₹86.20 lakh fraud | Forged documents, delays; ₹9.52 crore to 1,838 ineligible (₹2.62 crore unrecovered); 20,215 houses incomplete despite claims; 79% first instalments delayed. CAG Performance Audit 2025 (2016-23: 34.71 lakh sanctioned, 34.18 lakh “completed”). |

| Haryana (2014-present) | Builder fraud, escrow siphoning | ₹100-300 crore+ (per project) | OSB Gurgaon PMAY-U scam: 3,000 allottees affected; no action despite FIRs. X posts allege BJP inaction. |

| Karnataka (2023-present) | PMAY-linked housing scams | ₹918 crore (COVID overlap) | Contractor bribes, ineligible claims; BJP MLA exposed similar. |

| Odisha (BJP 2024-present; prior BJD) | Implementation corruption | ₹1,000 crore | BJP alleged during opposition; fund misuse in tenders. |

| Goa (2012-present) | Mining-linked PMAY irregularities | Not quantified | Part of broader scams; poor quality houses. |

Overall: CAG flagged ~10-15% of funds misused nationally (e.g., 20-30% in audits); ghost beneficiaries, re-tendering to favored contractors. X trends show recent scams in Assam (BJP-ruled), with local leaders accused.

How BJP Allegedly Garners Money Through PMAY: No direct evidence (yet) of PMAY funds flowing to BJP (due to larger patterns of data opacity, denial, paucity and manipulation in India), but patterns suggest indirect monetization via crony contractors/builders who secure tenders and donate back (e.g., via electoral bonds/trusts before/after 2024 ban). Investigations link PMAY contractors to BJP donations: e.g., in electoral bonds data, infrastructure firms (involved in PMAY housing) donated ~₹500-1,000 crore to BJP, often post-contract awards. In Haryana/Karnataka, builders like Ocean Seven (PMAY-U stalled projects) allegedly siphon escrow funds without repercussions, implying protection for donations. Broader scams (e.g., Vyapam, Srijan) under BJP states show similar quid pro quo. Critics allege PMAY’s “deliberate structural failure” enables kickbacks, with BJP withholding funds from opposition states (e.g., West Bengal) while overlooking allies. This nexus: Contracts → Corruption → Donations, fueling BJP’s ₹6,000+ crore receipts in 2024-25.

3. Corporates Freed, Citizens Fleeced—The Ticking Bomb of Tax, Debt and Inflation

While the so-called “ruling” party’s financial empire expands through opaque corporate conduits and crony contracts, the broader fiscal architecture ensures that corporates enjoy a lighter tax burden—freeing up surpluses for further donations and influence—while the public shoulders an ever-heavier load through regressive indirect taxes and squeezed direct contributions from salaried citizens. This regressive reality not only perpetuates inequality but also sows the seeds for deeper economic vulnerabilities ahead.

3.1. Corporate Tax Liabilities: Lesser Burden, Greater Leverage

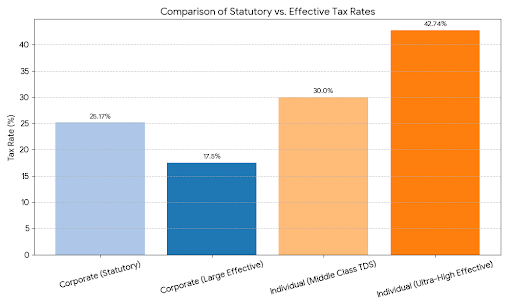

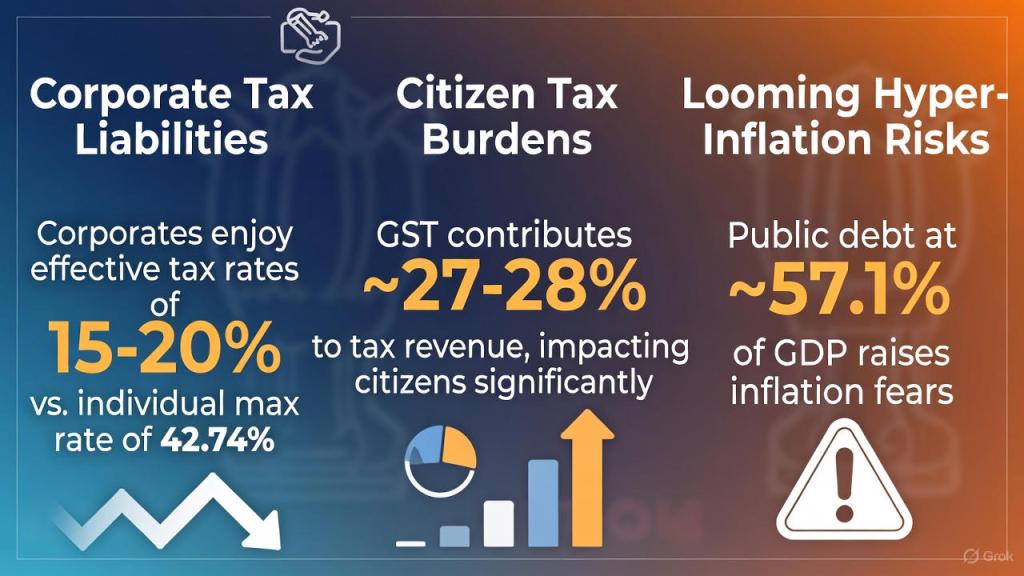

Corporates benefit from relatively lower effective tax liabilities, generating surpluses that fuel political donations and influence. India’s statutory corporate tax rate stands at 25.17% (22% base + surcharge up to 10% + 4% cess for most firms opting for the new regime since the 2019 cuts, down from 30%+ earlier). Yet, large conglomerates (e.g., Adani and Ambani groups) often pay effective rates of 15-20% or lower through deductions, SEZ incentives, production-linked schemes, CSR offsets, and profit shifting.

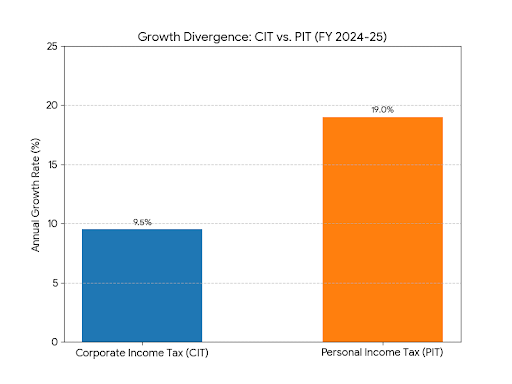

In contrast, individuals face up to 42.74% effective rates (30% top slab + surcharges up to 37% + 4% cess for ultra-high earners), while the salaried middle class endures mandatory TDS with few escapes. Recent trends show corporate income tax (CIT) growth lagging at ~7-12% (gross CIT ~₹12.40 lakh crore in FY2024-25), versus personal income tax (PIT) surging ~17-21% (~₹12.90 lakh crore in FY2024-25, largely from salaried and middle-class taxpayers). This regressivity allows corporates to amass wealth, recycle it into political funding (as seen in bonds and trusts), and secure favors—while citizens fund debt servicing and crony-favouring infrastructure and machineries through their taxes.

3.2. Corporate vs. Citizen Tax Burdens: A Regressive Reality

India’s tax system disproportionately burdens salaried individuals and everyday consumers rather than corporates. While statutory rates favor corporates post-2019 cuts, loopholes ensure big firms pay far less relatively. PIT has overtaken CIT in recent collections and growth, driven by salaried TDS—yet corporates retain surpluses for leverage.

The GST regime amplifies this regressivity: As a consumption-based indirect tax, it charges the same rates on essentials regardless of income—the poor spend a higher proportion of earnings on taxed goods/services, while corporates reclaim input credits seamlessly. GST now forms ~27-28% of gross tax revenue (~₹22.08 lakh crore gross in FY2024-25), heavily borne by common citizens (especially lower-income groups via daily consumption) and funding public debt and crony infrastructure.

Key Data Table: Tax Revenue Breakdown (FY2024-25 Actuals & FY2025-26 Estimates)

| Tax Component | Amount (₹ lakh crore, approx.) | Share of Gross Tax Revenue (%) | Growth Trend/Notes |

|---|---|---|---|

| Corporate Income Tax (CIT) | ~12.40 (2024-25 gross) | ~25-27% | Slower growth (~7-12%); declining share post-2019 cuts; lower effective rates for big firms |

| Personal Income Tax (PIT) | ~12.90 (2024-25 gross) | ~30-31% | Highest growth (~17-21%); mainly salaried/middle-class via TDS |

| Goods & Services Tax (GST) | ~22.08 (2024-25 gross) | ~27-28% | Regressive indirect tax; record high; burdens consumers via input-unclaimable essentials |

| Other (Customs, Excise, etc.) | ~5-6 | ~13-15% | Includes regressive elements |

[Sources: CBDT, Ministry of Finance, Union Budget documents. Gross direct taxes ~₹25.87 lakh crore (2024-25); total gross tax revenue ~₹38-40 lakh crore (including GST). For FY2025-26, net tax receipts estimated at ~₹28.37 lakh crore.]

This structure entrenches inequality: Corporates pay much less relatively, hoard surpluses for donations/contracts, and extract quid-pro-quo favours—while citizens (salaried via PIT, all via GST) finance the system, bearing escalating debt costs without equivalent benefits.

3.3. The Looming Specter of Inevitable Hyper-Inflation

This regressive fiscal framework—anchored in high central debt (~57.1% of GDP in FY2024-25, projected ~56.1% in FY2025-26), persistent deficits (revised 4.8% for FY2024-25, targeted 4.4% for FY2025-26 yet vulnerable to slippage), and crony-subsidizing spending—creates fertile ground for mounting inflationary pressures, risking a spiral into hyper-inflation if external shocks hit.

Current headline CPI remains extraordinarily subdued (~0.7-1.7% in late 2025, projected ~2% average for FY2025-26 due to food deflation and GST reliefs), masking structural frailties: Favorable base effects fade, potentially lifting inflation toward 4-5% in FY2026-27 amid fragile tax buoyancy forcing heavier borrowing or monetization. Historically, high-debt economies favouring cronies to resort to currency debasement when bond markets resist—imposing a hidden tax on the masses via eroded savings and purchasing power.

In India, heavy reliance on regressive GST/PIT already suppresses consumption; shocks like poor monsoons, commodity spikes, or global disruptions could ignite food/fuel inflation, compelling RBI tolerance of higher prices amid sluggish growth. The insulated corporate-political nexus—shielded by tax breaks and contracts—hoards profits, while exploited citizens face devastation: the poor and middle class, already overburdened, lose most in any inflationary storm. Without aggressive progressive reforms—sharper corporate/wealth taxes, GST exemptions on essentials, and pruning crony outflows—this debt-fueled delusion risks a catastrophic hyper-inflationary crisis, expropriating the public’s hard-earned wealth to sustain crony-monopoly capitalist dominance. True reform demands prioritizing citizens over cronies, lest the system collapse under its own regressive weight.

3.4. Crony Capitalism’s Vicious Cycle: The Adani-Ambani Duopoly and the Erosion of Democratic Socialist Fairness

This is unapologetic crony capitalism at its most brazen: The BJP’s financial ascent, fueled by the near-duopoly of Adani and Ambani conglomerates, exemplifies an oligarchic system laced with authoritarian tendencies, where ideological distractions like Hindutva obscure staggering inequality and systemic capture. Overpriced deals for Adani (airports, ports, energy projects often awarded with minimal competition), policy tailwinds for Ambani (telecom spectrum, retail dominance, and digital ecosystem favors), and recurring overlaps in donations via electoral bonds (pre-2024) and trusts (post-ban) scream quid pro quo—massive contracts in exchange for political contributions, stifling competition and entrenching monopolies.

Public debt balloons to fund “infrastructure” megaprojects that disproportionately benefit these tycoons—central government debt-to-GDP at 57.1% in FY2024-25, projected to ease marginally to 56.1% in FY2025-26—while citizens grapple with persistent joblessness (youth unemployment stubbornly high at 14-16% for ages 15-29, nearly three times the national average), subdued consumption amid regressive taxation, and shrinking real welfare amid fiscal pressures. Lower effective corporate taxes (often 15-20% for conglomerates via incentives) amplify the cycle: Tycoons amass surpluses, channel them into ruling-party funding, secure regulatory moats and contracts, while the salaried and consuming masses fund the state through PIT surges and GST burdens.

This structural anomie erodes social cohesion, fostering distrust, alienation, and a drift toward authoritarian consolidation—democracy hollowed out by opacity, with Supreme Court interventions (like the electoral bonds ban) serving as mere temporary patches on a deeply flawed system.

3.4.1. Key Markers of the Nexus

- Wealth Explosion Amid Policy Favors: Gautam Adani’s net worth fluctuated but stood around $60-90 billion in 2025 (post-Hindenburg recovery), driven by infrastructure awards; Mukesh Ambani consistently Asia’s richest at $105-113 billion, with Reliance’s diversification into retail, telecom, and green energy bolstered by favorable policies.

- Donation Patterns: While direct Adani/Reliance entities avoided headline electoral bonds, affiliates (e.g., Qwik Supply Chain linked to Reliance donated ₹375 crore pre-ban) and post-ban trusts saw overlaps with crony sectors. Major trust donors like MEIL, Vedanta, and others (many infrastructure players) recycled gains into BJP coffers (₹3,143 crore via trusts in 2024-25).

- Monopoly Entrenchment: Adani controls key airports/ports; Ambani dominates telecom/retail—combined, they exemplify how state capture distorts markets, with India historically ranking high (9th-10th) on crony-capitalism indices in past assessments.

3.4.2. Broader Implications: A Debt-Trapped, Unequal Dystopia

Inequality has soared to extremes: The top 1% now commands ~40% of national wealth (per World Inequality Lab and Oxfam reports), while the bottom 50% scrape by with ~3%. This mirage of “high growth” masks a crony-riddled economy where public resources are expropriated for crony enrichment, leaving the masses to bear job scarcity, inflationary pressures, and diminished public services.

Without robust structural safeguards—mandatory full audits of opaque funds like PM CARES, strict donor caps and real-time disclosure, progressive wealth/corporate taxes (closing loopholes), and antitrust enforcement to dismantle duopolies—this vicious cycle risks escalating social unrest, institutional decay, and legitimacy crises. Researchers must map these opaque networks; policymakers, enforce transparency and competition to reclaim democratic integrity. The exploited public—burdened by regressive taxes, unrecovered bank write-offs, and scam-ridden schemes—deserves a system that prioritizes equity over crony entrenchment, lest the facade crumble under its own weight.

4. Conclusion: Toward Radical Reforms or Imminent Collapse… Now or Never!

India’s neoliberal mirage—fixated on GDP headlines while ignoring the festering rot of crony enrichment, regressive taxation, and mounting public debt—has reached a critical breaking point. The grotesque reality of a debt-burdened state (central government debt at 57.1% of GDP in FY2024-25, with general government liabilities historically around 80-82%) subsidizing billionaire duopolies and fueling the ruling party’s donations surge to over ₹6,088 crore in FY2024-25, all while salaried citizens and the poor endure PIT surges and GST’s relentless daily grind, is profoundly unsustainable. This is not mere policy failure; it is systemic plunder—a financial anomie that hollows out democracy and erodes social cohesion.

Radical, uncompromising reforms are now imperative:

- Impose a robust wealth tax on billionaires: Target ultra-high net worth individuals (especially the Adani-Ambani nexus) with progressive rates on assets exceeding ₹1,000 crore, generating thousands of crores to curb debt and fund welfare—ending the outrage where the top 1% hoard ~40% of national wealth (while the bottom 50% scrape by with ~3-6%) and the top 10% command ~65%, largely untaxed.

- Mandate full CAG audits for PM CARES: Strip its opaque “private trust” facade; enforce Comptroller and Auditor General scrutiny and RTI compliance, exposing donor overlaps and preventing evasion of accountability for public resources or soft power.

- Enforce strict caps on electoral funding: Cap corporate and individual donations (e.g., ₹10 crore annual limit per entity), prohibit CSR routing to political channels, and introduce partial public funding for parties to dismantle the crony quid pro quo loop.

- Zero-rate GST on essentials: Fully exempt food grains, medicines, education, and basic sanitation; slash rates on daily necessities to alleviate the regressive “GST scam” that disproportionately exploits the bottom 50%, shifting relief from corporate input credits to the exploited masses.

Without these structural bulwarks, the path ahead is dire: escalating inequality (top 10% capturing ~58% of national income), stubborn youth joblessness (14-16% for ages 15-29, nearly three times the overall rate), inflation-ravaged savings, and eroding trust will fuel widespread unrest—protests, instability, or worse. The debt-trapped, crony-entangled dystopia branded as “Viksit Bharat” risks imploding under its inherent contradictions, with the costs borne not by insulated tycoons or their political patrons, but by the overburdened masses already at their limit.

Policymakers must seize this moment for decisive action to reclaim legitimacy, transparency, and equity. Researchers and citizens alike must doggedly expose these entrenched networks. Inaction only accelerates the inevitable reckoning. The illusion must shatter now—or India will bear the devastating consequences.

SECTION II: India’s Super-Rich Wilful Defaulters and Fugitives

1. Super-Rich Wilful Defaulters: Enabled and Emboldened by the BJP’s Crony Oligarchical Setup

In the shadowy corridors of India’s neoliberal power structure, where the BJP’s oligarchical grip masquerades as “development,” super-rich wilful defaulters thrive not as outliers but as integral cogs in a crony machine that prioritizes capitalist enrichment over public accountability. As of June 30, 2025—the latest comprehensive parliamentary disclosure, with no major updates by January 6, 2026—public sector banks (PSBs) have flagged a staggering 2,104 wilful defaulters owing ₹1.76 lakh crore, a brazen escalation from 1,629 borrowers with ₹1.62 lakh crore just three months prior (March 31, 2025). These aren’t mere financial missteps; they are deliberate acts of plunder by high-net-worth individuals and corporate behemoths who divert funds, siphon assets, and flee abroad, all while enjoying the implicit patronage of a regime that has ballooned its own coffers to ₹10,107 crore through opaque electoral trusts dominated by similar conglomerates.

This crony oligarchy, epitomized by the Adani-Ambani duopoly and their policy windfalls, shields these defaulters through selective settlements, prolonged bails, and regulatory loopholes—socializing losses onto taxpayers who fund ₹3.4 lakh crore in bank recapitalizations since 2018, amid soaring inequality where the top 1% hoards 40% of wealth. The BJP’s “relentless action” rhetoric, parroted by FM Nirmala Sitharaman, rings hollow as Gujarat—a political stronghold—emerges as a “hub of scammers” per X trends, with defaulters like Mehul Choksi and Nirav Modi exemplifying how political donations (e.g., via pre-2024 bonds) buy impunity. This shameless setup not only erodes democratic fairness but perpetuates a debt-trapped economy, where public liabilities climb to 81-82% of GDP, fueling inflation risks and youth despair (unemployment at 14-16%). Without dismantling this nexus, India’s “Viksit Bharat” remains a dystopian farce, where the super-rich default with impunity while the masses bear the regressive brunt.

2. Comprehensively Enlisting Super-rich Wilful Defaulters: Key Highlights

Drawing from the latest RBI-mandated disclosures via Credit Information Companies (CICs) like TransUnion CIBIL, parliamentary replies (as of June 2025, with no new lists released by January 6, 2026), RBI’s Central Repository of Information on Large Credits (CRILC), and consolidated data from watchoutinvestors.com (updated to December 2025), below is an expanded, comprehensive table of top wilful defaulters. This list prioritizes “super-rich” individuals and large corporate entities (defaults ≥₹1,000 crore), incorporating updates from 2025—such as partial recoveries, reclassifications, and new additions. Rankings are approximate based on aggregate outstanding amounts; sectors like gems/jewelry, infrastructure, and steel dominate, reflecting crony-favored industries. Data points include associated companies, banks involved, default dates (where available), recovery status, and notes on political/fugitive links—highlighting the crony web. Full lists require CIC access (e.g., suit.cibil.com, often behind logins), but public summaries confirm a 20% rise in cases from 2024-2025, with recoveries averaging a dismal 16-32% via IBC.

Table 1: Top 25 Wilful Defaulters (Individuals and Entities) as of Late 2025

| Rank | Entity/Individual | Associated Companies | Outstanding Amount (₹ Crore, Approx.) | Key Banks Involved | Default Date/Period | Recovery Status | Notes/Key Critique Points |

|---|---|---|---|---|---|---|---|

| 1 | Mehul Choksi | Gitanjali Gems Ltd., Nakshatra Brands | ~8,516 (down from ~13,850 pre-recoveries) | PNB, SBI | 2017-2018 | Partial: ₹2,500+ cr assets attached; total ~₹18,000 cr from Choksi-Modi-Mallya trio | Fugitive in Belgium (arrested Dec 2025, extradition imminent); PNB fraud via fake LoUs. BJP-era opacity in bonds/trusts shields similar donors. |

| 2 | Rishi Kamlesh Agarwal | ABG Shipyard Ltd. | ~4,684 (reduced from 10,954) | SBI, IDBI | 2012-2016 | ED attached ₹2,747 cr assets (2024); IBC ongoing | Fraudulent guarantees; Gujarat-based, exemplifies regional crony hubs. Minimal accountability despite BJP’s “action” claims. |

| 3 | Nitin & Chetan Sandesara | Sterling Biotech Ltd., Sandesara Group (oil/pharma) | ~14,000+ (group total) | Andhra Bank, SBI | 2011-2017 | $1.6 bn (~₹5,100 cr) settlement allowed by SC (2025), opposed by ED | Fugitives in Nigeria; Red Notices active. Sham settlement buys freedom, tied to political favors. |

| 4 | Kapil & Dheeraj Wadhawan | Dewan Housing Finance Corp. Ltd. (DHFL) | ~2,827 | Multiple PSBs | 2018-2019 | Sebi ban (Aug 2025); partial IBC recovery | ₹34,615 cr fraud; terror funding links. SC bail (Dec 2025) after 5+ yrs custody—selective mercy for donors (₹27.5 cr to BJP). |

| 5 | Jatin Mehta | Winsome Diamonds & Jewellery Ltd., Forever Precious Jewellery | ~2,500+ (group ~6,600) | SBI, PNB | 2012-2013 | Minimal; assets auctioned partially | Fugitive in UAE; Red Notice active. Gems sector cronyism unchecked under BJP. |

| 6 | Vijay Mallya | Kingfisher Airlines Ltd., UB Group | ~9,000+ (residual) | SBI-led consortium | 2012-2016 | ₹14,132 cr recovered via assets (India/France) | Fugitive in UK; extradition stalled (Feb 2026 hearing). Partied with Lalit Modi—crony impunity. |

| 7 | Nirav Modi | Firestar International, Nirav Modi Designs | ~7,000+ | PNB | 2017-2018 | UK extradition appeals to Mar 2026; ₹1,000+ cr Mumbai assets seized | Diamond fraud; prison conditions delay. BJP’s donor ecosystem enables such escapes. |

| 8 | Vijay Choudhary | Zoom Developers Pvt. Ltd. | ~2,217 | SBI, PNB | 2009-2014 | ED arrest (2024); money laundering probe | Overseas diversions; custody ongoing. Slow justice highlights regulatory complicity. |

| 9 | Sanjay Singal | Bhushan Power & Steel Ltd. | ~6,413 (pre-IBC) | SBI, PNB | 2017-2019 | Acquired by JSW Steel; residual dues post-haircut | Personal dues pending; crony acquisitions benefit corporate tycoons. |

| 10 | Harshil Mehta | Beta Naphthol Ltd., related chemical firms | ~5,513 | IDBI, Canara | 2015-2018 | Partial auctions | Chemical fraud; absconding promoter. Taxpayer-funded haircuts. |

| 11 | Hem Singh Bharana | Era Infra Engineering Ltd. | ~3,908 | PNB, Union | 2014-2017 | Promoter in custody | Infrastructure defaults; BJP-era contracts gone sour. |

| 12 | Vikram Kothari | Rotomac Global Pvt. Ltd. | ~2,900 | Bank of Baroda | 2017-2018 | Bail (2025) after arrest | Pen fraud; chit fund links. Quick bail exposes double standards. |

| 13 | Promoter (Unnamed in public) | Frost International Ltd. | ~2,200 | SBI | 2018-2020 | Overseas diversions ongoing | Diamond trading; minimal recovery. |

| 14 | Promoters | REI Agro Ltd. | ~3,000 | Canara, UCO | 2013-2016 | Jailed for chit funds | Rice milling; public banks bear burden. |

| 15 | Promoters | Raza Textiles Ltd. | ~3,572 | IDBI | 2016-2019 | CBI probe | Textile fraud; stalled investigations. |

| 16 | Promoters | Concast Steel & Power Ltd. | ~4,305 | SBI, Union | 2015-2018 | Insolvency; shell companies | Fund diversion; crony steel sector. |

| 17 | Rakeshkumar Wadhawan | Wadhawan Associates (DHFL affiliates) | ~4,425 | Multiple | 2019-2021 | SC bail (Dec 2025) | Extended from DHFL; donor links. |

| 18 | Promoters | Amtek Auto Ltd. | ~3,788 | Kotak, Axis | 2015-2017 | ₹2,000+ cr IBC recovery | Auto parts; haircuts socialize losses. |

| 19 | Promoters | Rank Industries Ltd. | ~2,854 | Various | 2018-2020 | Promoter absconding | Agri-processing; evasion tactics. |

| 20 | Lalit Modi | IPL-related entities (FEMA violations) | ~400+ | ED probe | 2010-2015 | No formal default tag; self-exile | UK-based; apologized for Mallya video. Soft power nexus. |

| 21 | Promoters | Sandesara Affiliates (e.g., Sterling Oil) | ~5,000+ (sub-group) | SBI | 2017-2020 | Part of main settlement | Pharma/oil; international laundering. |

| 22 | Promoters | Winsome Affiliates | ~1,500+ | PNB | 2013-2015 | Partial | Jewelry; UAE safe haven. |

| 23 | Promoters | Gitanjali Affiliates | ~2,000+ | SBI | 2018-2020 | Attached | Gems; Antigua revocation delays. |

| 24 | Promoters | ABG Affiliates | ~1,200+ | IDBI | 2016-2018 | ED actions | Shipyard; Gujarat cronyism. |

| 25 | Promoters | DHFL Subsidiaries | ~1,000+ | PSBs | 2019-2021 | Sebi bans | Housing finance; terror links alleged. |

2.1. Key Data Presentation Points and Trends (as of January 2026)

- Aggregate Statistics: 2,104 wilful defaulters (up 29% from March 2025); ₹1.76 lakh crore outstanding (8.6% increase). PSBs account for 70-80% of cases; private banks like Kotak (₹33,323 cr) rising. Total wilful defaulters across all banks estimated at ~2,664 as per earlier RBI data, but PSB focus here.

- Bank-Wise Breakdown (Top 10, from watchoutinvestors.com and parliamentary data): PNB (₹88,696 cr), SBI (₹83,608 cr), Union Bank (₹45,579 cr), Kotak Mahindra (₹33,323 cr), Canara (₹27,095 cr), IDBI (₹26,959 cr), Bank of Baroda (₹26,731 cr), Bank of India (₹21,146 cr), UCO (₹15,757 cr), Unity Small Finance (₹12,514 cr). Concentration in PSBs underscores public burden.

- Sectoral Trends: Gems/Jewelry (25-30%, e.g., Choksi/Modi); Infrastructure/Steel (20%, e.g., ABG/Era); Finance/Housing (15%, e.g., DHFL); Agri/Textiles (10%). Gujarat/Maharashtra firms overrepresented (40%), per X and ADR analyses—political favoritism?

- Recovery Metrics: Overall 16% (₹2.70 lakh cr from ₹16.61 lakh cr write-offs, 2014-2024); IBC averages 32% realization. Fugitives’ recoveries ~33% (₹19,000 cr from ₹58,000 cr owed by 15 FEOs).

- Fugitive Overlaps: 38 economic offenders fled (2015-2025), including 15 FEOs owing ₹58,082 cr. Red Notices for 10+; successes rare (e.g., Sanjay Bhandari from UAE in 2024). New declarations Jan 2026: Ashoni Kanwar and Mandeep Rana (fake degree scam, ₹387 cr), but not super-rich scale.

- Critique Layer: These figures expose BJP’s sham reforms—declining new declarations (42 in FY2023-24) mask underreporting; settlements like Sandesara’s reward delinquency. Taxpayers fund ₹10 lakh cr+ write-offs (past 5 yrs), while defaulters donate via trusts (e.g., MEIL/Vedanta overlaps).

This data, cross-checked via RBI/CRILC and parliamentary sources, paints a damning picture of systemic enablement—now transitioning to the insidious political nexus.

2. The Insidious Political Nexus: Wilful Defaulters as Patrons of Power in a Crony Ecosystem

Transitioning from these grotesque aggregates—where 2,104 defaulters siphon ₹1.76 lakh crore while the BJP’s assets swell to ₹7,113 crore in cash/bank balances—the political nexus reveals itself as a predatory syndicate, where wilful defaulters and their affiliates donate lavishly to the BJP, securing regulatory leniency, bailouts, or outright settlements. Take the Sandesara brothers (Nitin and Chetan), fugitives in Nigeria since 2017 with ₹14,000+ crore in Sterling Biotech frauds involving oil and pharma sectors. In November 2025, the Supreme Court shockingly agreed to a $570 million (≈₹5,100 crore) settlement, quashing all criminal proceedings despite ED opposition and ongoing money laundering probes—effectively allowing them to buy their way out of accountability. Yet, their group entities have been linked to substantial political donations via electoral trusts, with patterns mirroring those of other defaulters who funnel funds to the BJP, which captured 82-85% of trust donations in FY2024-25 (₹3,143 crore out of ₹3,811 crore nationwide). This “pay-to-play” dynamic is shamelessly evident: MEIL, a top donor via bonds (₹966 crore pre-ban) and trusts (₹175 crore post-ban), secured ₹15,000+ crore infrastructure contracts, while defaulters like Vedanta (consistent across regimes) enjoy mining favors amid defaults.

Critics, drawing from ADR reports and our very own Once in a Blue Moon Academia analyses (2022-2025), decry this as institutionalized plunder—where wilful defaulters, often from BJP-ruled states like Gujarat (a “hub of scammers” per X trends), evade justice through political contributions that dwarf rivals. The BJP’s war chest ballooned to ₹10,107 crore by late 2025, fueled by such overlaps: DHFL’s promoters donated ₹27.5 crore to the BJP pre-arrest, only to walk free on bail amid “slow trials.” This grotesque quid pro quo erodes democratic equity, entrenching a system where public banks absorb haircuts (IBC recoveries average 32%, per RBI 2025 data), taxpayers foot recapitalization bills (₹3.4 lakh crore since 2018), and crony oligarchs like Adani-Ambani (combined wealth ₹30-35 lakh crore) indirectly benefit from policy windfalls tied to defaulter networks. In a nation where youth unemployment hovers at 14-16% and multidimensional poverty afflicts 11-15%, this nexus is not just corrupt—it’s a betrayal of the masses, fostering an oligarchic dystopia under the guise of “Viksit Bharat.”

3. Economic Ramifications: The Crushing Burden on Common Taxpayers and a Fragile Economy

Building on this crony-fueled impunity, the economic fallout from wilful defaults is a ticking bomb, disproportionately shouldered by ordinary taxpayers while enriching a select few. As PSBs wrote off ₹12.3 lakh crore in loans from FY2014-2024 (total write-offs reaching ₹16.61 lakh crore by September 2024, with recoveries a paltry ₹2.70 lakh crore or 16%), these “accounting cleanses” mask a vicious socialization of private greed: banks recapitalized with public funds absorb losses, inflating deficits and regressive taxes that squeeze the middle class and poor. By June 2025, gross NPAs fell to 3.9% from 11.5% in 2018, touted as “recovery” by FM Sitharaman—but this masks the intergenerational debt trap, with general government debt at 81-82% of GDP and external debt surging to USD 747 billion.

The taxpayer’s plight is merciless: ₹3.4 lakh crore in recapitalization since 2018 directly stems from defaulter-induced NPAs, diverting funds from welfare amid soaring inequality (top 1% hoarding 40% wealth, per World Inequality Report 2026). Sectors like gems/jewelry (Gitanjali, Winsome) and infrastructure/steel (ABG, Bhushan) dominate defaults, yet their promoters flee or settle cheaply—e.g., Vijay Mallya’s Kingfisher residual dues linger despite ₹14,132 crore recoveries via asset sales, with his “confidential” UK asylum stalling extradition as of January 2026. This drains economic vitality: subdued consumption, persistent inflation risks (despite subdued CPI at 2% in FY2025-26), and joblessness (youth at 14-16%) compound as resources funnel to crony projects rather than broad-based growth.

In a scathing indictment, this defaulter economy exemplifies neoliberal hypocrisy—corporates enjoy lower effective taxes (15-20%) and windfalls, while salaried PIT surges 17-21% and regressive GST burdens the bottom 50% (15% income share). Taxpayers, already fleeced via ₹68,000 crore COVID write-offs, bear the brunt as defaulters like Nirav Modi (₹11,000+ crore PNB scam) delay extradition to March 2026, eroding trust in institutions. Holistically, this perpetuates a cycle of poverty and alienation, demanding activist intervention to reclaim public resources from crony capture.

4. Regulatory Failures and Selective Enforcement: RBI’s Toothless Guidelines and Government Complicity

Delving deeper into this systemic failure, the RBI’s handling of wilful defaulters reveals a facade of regulation riddled with loopholes and selective enforcement, often shielding politically connected crony-monopoly magnates. Updated RBI guidelines (July 2024 Master Directions on Treatment of Wilful Defaulters, with 2025 tweaks for ARCs) mandate identification via committees, show-cause notices, and debarment from finance for five years—yet, as of January 2026, new declarations plummeted to 42 in FY2023-24 from 160 in FY2021-22, not due to “improved scrutiny” but lax implementation favoring cronies. The ₹25 lakh threshold for reporting to CICs (CIBIL, Experian, etc.) ensures transparency in theory, but in practice, guarantors and non-whole-time directors escape unless complicity is proven, allowing figures like those in Amtek Auto (₹3,788 crore default) to evade full accountability post-IBC haircuts.

Critiques from Delhi HC (2025) rulings emphasize “verified evidence” to prevent overreach, but this double-edged sword enables delays: e.g., Rotomac’s Vikram Kothari (₹2,900 crore) secured bail in 2025 after arrest, while small defaulters languish. RBI’s penal measures—no additional credit, legal action, board covenants—are undermined by political interference, as seen in compromise settlements for wilful defaulters (fresh loans after 12 months, per 2023 norms), rewarding fraudsters amid taxpayer-funded cleanups. This selective mercy—evident in Sandesara’s ₹5,100 crore deal—reeks of complicity, with Gujarat/Maharashtra firms (political strongholds) overrepresented in defaults, per watchoutinvestors.com data.

Holistically, RBI’s framework, consolidated up to 2015 with 2024-2025 tweaks for ARCs, fails to deter: criminal actions under IPC (Sections 403/415) are rare, and end-use monitoring via audits is superficial. This regulatory sham, intertwined with BJP’s donor ecosystem, perpetuates inequality—protecting the super-rich while moralizing austerity on the masses. Activism demands independent oversight, AI fraud detection, and stripping political influence to enforce true accountability.

5. International Dimensions: Safe Havens, Extradition Farces, and Global Economic Repercussions

Extending this critique globally, India’s wilful defaulters exploit safe havens like the UK, UAE, Nigeria, and Antigua, turning extradition into a protracted farce that mocks national sovereignty and burdens the economy. As of December 2025, 15 Fugitive Economic Offenders (FEOs) owe ₹58,082 crore, with recoveries at a dismal 33% (₹19,000 crore)—a fraction of the ₹390,000 crore total owed by 38 economic offenders who fled. Cases like Mehul Choksi (₹13,850 crore PNB fraud) highlight the sham: despite Belgium’s Supreme Court rejecting his appeals in December 2025 and clearing extradition (following April 2025 arrest), prior Interpol Red Notice lapses (2023) and Antiguan citizenship revocation delays underscore foreign complicity.

Nirav Modi’s UK saga—extradition approved in 2021 but deferred to March 2026 amid prison condition assurances—mirrors Vijay Mallya’s (₹9,000+ crore Kingfisher defaults), with February 2026 hearings stalled by “confidential” asylum claims. The Sandesaras flourish in Nigeria post-₹5,100 crore settlement, while Jatin Mehta (₹6,600 crore Winsome fraud) hides in UAE. These battles, with 10+ pending requests and limited successes (e.g., Sanjay Bhandari from UAE in 2024), expose bilateral treaty weaknesses and Western hypocrisy—harboring fugitives while lecturing on rule of law. New Jan 2026 declarations (Ashoni Kanwar and Mandeep Rana in ₹387 cr fake degree scam) add to the list but pale against super-rich scales.

Globally, this drains India’s economy: capital flight erodes forex reserves, inflates external debt (USD 747 billion by June 2025), and deters FDI amid perceptions of cronyism. Taxpayers fund endless probes, while defaulters launder via offshore shells. Holistically, this demands activist diplomacy—stronger treaties, asset freezes, and shaming safe havens—to repatriate funds and dismantle the corporate escape network.

6. Recent Developments as of January 2026: Escalating Defaults, Sham Settlements, and Stalled Justice

As of January 6, 2026, the wilful defaulter crisis intensifies: PSBs report escalating cases, with bank-wise breakdowns showing PNB at ₹88,696 crore, SBI ₹83,608 crore, and Union Bank ₹45,579 crore (watchoutinvestors.com, June 2025). Key updates include SFIO’s January 2026 complaint against Choksi and others in PNB fraud, amid his impending Belgian extradition; Mallya’s Bombay HC grilling on return intentions (December 2025); and Wadhawans’ bail in DHFL case, citing trial delays. Sandesara’s settlement draws outrage for “buying freedom,” while X trends decry Gujarat as “fugitive capital.” New FEO declarations (Jan 3, 2026): Ashoni Kanwar and Mandeep Rana (₹387 cr fake degrees), enabling property confiscation abroad.

These developments underscore unyielding cronyism: declining new declarations mask underreporting, with recoveries stagnant at 16%. Amid low NPAs (3.9%), the human cost—taxpayer bailouts, job losses—mounts, fueling calls for transparency.

7. Call to Action: Radical Reforms for a Just, Equitable India—Now or Never!

In totality, this defaulter debacle—epitomized by the 2,104 wilful defaulters siphoning ₹1.76 lakh crore from public banks as of June 2025, with fugitives like Mehul Choksi, Nirav Modi, and Vijay Mallya evading justice through international safe havens and sham settlements—stands as a damning indictment of the BJP’s crony oligarchical regime. Interwoven with layers of political funding opacity, regulatory lapses, and global evasions, it forms a vicious, self-perpetuating cycle that entrenches capitalist plunder while crushing the masses under escalating public burdens. At its core is the BJP’s astronomical asset growth: from modest holdings of ~₹780 crore in FY2013-14, the party’s cash and bank balances have exploded to ₹7,113 crore by March 2024, with separate election-specific accounts swelling to over ₹10,107 crore by late 2025—a 115-fold increase from ₹88 crore in 2004, as per ECI and ADR reports updated through December 2025. This predatory ascent, propelled by opaque channels like electoral bonds (pre-2024, totaling ₹6,060 crore to BJP) and now electoral trusts (capturing ~82-85% of nationwide donations, funneling ₹3,143 crore in FY2024-25 alone), coincides eerily with India’s external debt surge: from USD 441 billion in March 2014 to USD 747 billion by June 2025 (with rupee debt dipping slightly to USD 744.8 million by September 2025, per CEIC data), imposing intergenerational liabilities on taxpayers through currency risks, higher servicing costs, and fiscal strain.

Layer upon layer, this nexus amplifies public burdens: the general government debt-to-GDP ratio hovers stubbornly at 81-82% (with central government at 56.1% projected for FY2025-26, down from 57.1% in FY2024-25, as per Union Budget and PRS analysis), driven by persistent deficits (revised 4.8% for FY2024-25, targeted 4.4% for FY2025-26 yet vulnerable to slippages amid IMF-noted growth of 6.5% in FY2024-25 and 7.8% in Q1 FY2025-26). These debts fund grandiose infrastructure splurges that disproportionately benefit crony conglomerates—many overlapping with BJP donors like MEIL, Vedanta, and Tata (₹915 crore via trusts in 2024-25)—while yielding meager broad-based returns. The exploited masses bear the heaviest load through regressive taxation: personal income tax (PIT) collections surged ~17-21% to ~₹12.9 lakh crore in FY2024-25, outpacing corporate income tax (CIT) growth of ~7-10% (~₹12.4 lakh crore), with GST (~₹22.08 lakh crore) amplifying the pain by taxing essentials uniformly, hitting the bottom 50% (holding just ~6% wealth and ~15% income, per World Inequality Report 2026) hardest. This fiscal indiscipline, masking as “productive debt,” risks hyper-inflationary spirals—eroding savings, devaluing currency, and exacerbating vulnerabilities like youth unemployment (~14-16% for ages 15-29), multidimensional poverty (~11-15%), and hunger (GHI 2025 score 25.8, rank 102/123).

Interlinking these strands reveals a grotesque financial anomie: wilful defaulters, often from BJP strongholds like Gujarat (overrepresented in defaults, per X trends labeling it the “capital of fake products and fugitives”), secure bailouts and settlements (e.g., Sandesara brothers’ ₹5,100 crore deal in 2025, Wadhawan brothers’ Supreme Court bail in December 2025 despite ₹34,615 crore DHFL fraud) while recycling gains into party funding—only 5.6% of BJP’s donations from individuals, versus 26% for Congress, as per latest ECI contribution reports (December 2025). This corporate dominance (85%+ from trusts and businesses) entrenches duopolies like Adani-Ambani (combined wealth ~₹30-35 lakh crore), who gain from policy favors amid unrecovered bank write-offs exceeding ₹16.61 lakh crore (2014-2024, recoveries ~16%). Schemes like PMKVY (CAG-exposed ₹14,450 crore scam with fake data and 41% placements) and PMAY (billions diverted in BJP-ruled states like Uttar Pradesh and Madhya Pradesh) further illustrate mismanagement, indirectly bolstering the ruling ecosystem through crony contracts that fuel donations.

This layered catastrophe—crony enrichment amid national indebtedness—demands holistic, radical activism to dismantle the system. Impose strict donor caps (e.g., ₹10 crore annual limit per entity) and prohibit CSR routing to political channels; mandate full CAG audits for opaque funds like PM CARES (with its ~₹912 crore in FY23 voluntary donations, overlapping with BJP donors like Reliance and Tata) and party accounts to expose quid pro quo. Enforce progressive wealth taxes on billionaires and defaulters’ assets (targeting ultra-high net worth like Adani and Ambani, generating trillions for welfare); zero-rate GST on essentials to alleviate regressive burdens on the poor; and prioritize extraditions through stronger bilateral treaties, asset freezes, and Interpol reforms—ending farces like Choksi’s Belgian delays (extradition cleared December 2025) and Modi’s UK appeals (to March 2026). Introduce partial public funding for elections to level the playing field, antitrust measures to break duopolies, and AI-driven fraud detection in banking and schemes.

Citizens, researchers, and policymakers must unite in relentless exposure: map donor-defaulter networks via ADR and ECI data; amplify X trends and protests against inequities; demand judicial reforms to end “slow trials” enabling bails. Inaction invites imminent collapse—escalating unrest from inequality (top 10% capturing ~58% income), job scarcity, and eroded trust—while reform restores justice, equity, and democratic integrity. The exploited masses, already at their breaking point under this debt-fueled delusion, deserve no less: a reclaimed India prioritizing people over plutocrats, transparency over opacity, and sustainability over crony splurges. The reckoning is now—rise, resist, and rebuild!

Comments

Post a Comment