When AA+ Means “Ask Again”: Manufactured Ratings, Piramal Finance, and the Credit Ratings Trap

When AA+ Means “Ask Again”: Manufactured Ratings, Piramal Finance, and the Credit Ratings Trap

Posted on 6th January, 2026 (GMT 01:36 hrs)

Authored by DHFL Victim⤡

ABSTRACT

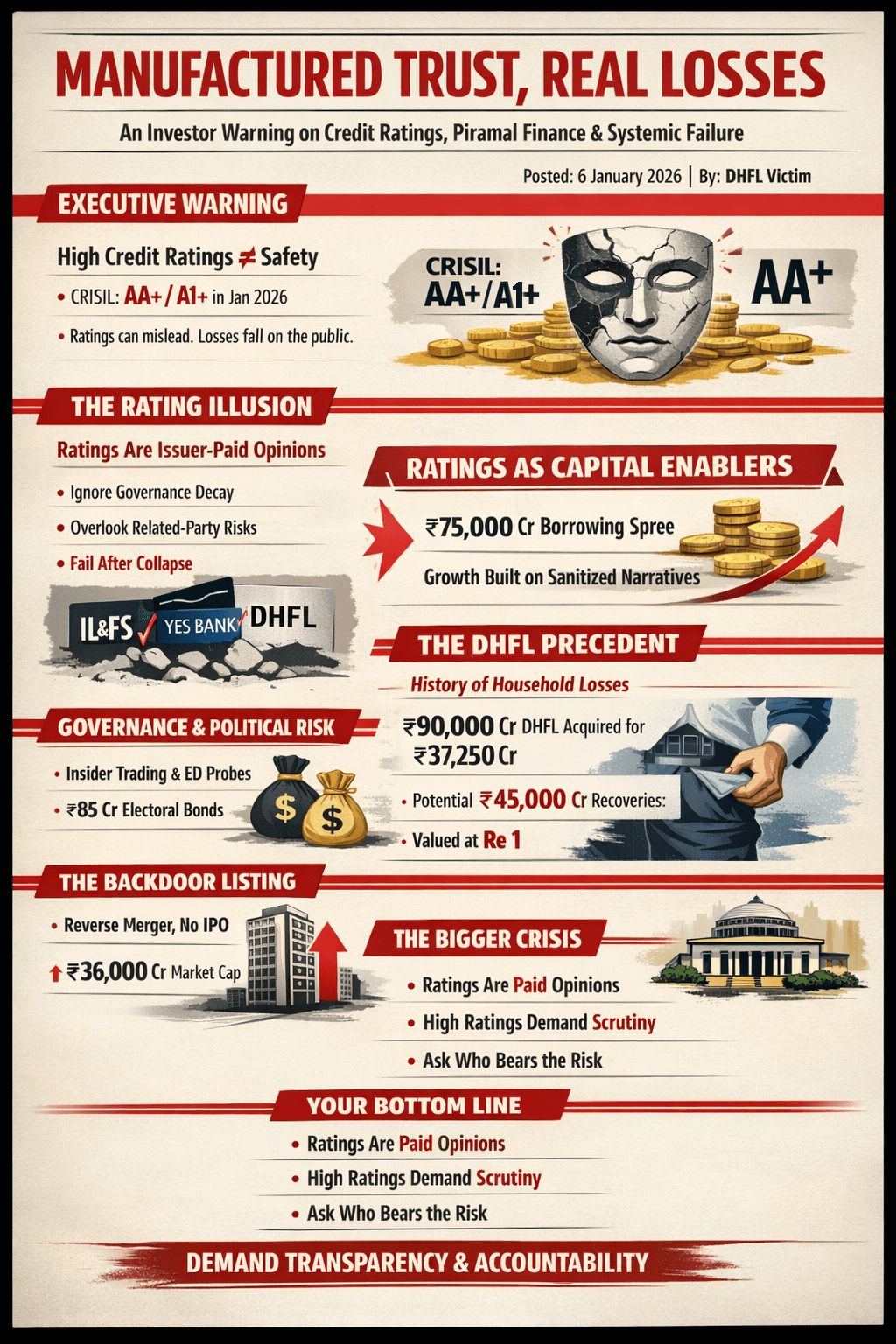

Despite glowing CRISIL AA+/Stable ratings, Piramal Finance’s strength is an illusion built on conflicted issuer-paid ratings, legacy DHFL fraud asymmetries (₹45,000 Cr recoveries valued at Re 1, massive retail haircuts), governance controversies, political proximity, and a backdoor listing that bypassed scrutiny. High ratings enable cheap funding and retail mobilisation—while systematically ignoring forensic risks, related-party issues, and resolution inequities seen in IL&FS, Yes Bank, DHFL. This is systemic: manufactured trust, socialised losses, privatised gains. Ratings are opinions, not guarantees. Demand truth before investing.

A Call to Investors, Depositors, and Market Participants

Executive Warning – Piramal Finance:

Executive Warning – Piramal Finance:

High Ratings ≠ Safety

Investor Alert – January 2026

Investor Alert – January 2026

Piramal Finance currently enjoys  CRISIL AA+/Stable (long-term) & A1+ (short-term) ratings — widely seen as a sign of strength. Yet this polished narrative hides a troubling reality:

CRISIL AA+/Stable (long-term) & A1+ (short-term) ratings — widely seen as a sign of strength. Yet this polished narrative hides a troubling reality:  manufactured trust,

manufactured trust,  socialised losses,

socialised losses,  privatised gains.

privatised gains.

Core Message in 12 Key Points

Core Message in 12 Key Points

Ratings are not independent

Ratings are not independent  Issuer-pays model + oligopoly (CRISIL, ICRA, CARE) creates inherent conflict of interest.

Issuer-pays model + oligopoly (CRISIL, ICRA, CARE) creates inherent conflict of interest. Ratings heavily rely on

Ratings heavily rely on  Management narrative, issuer disclosures, short-term metrics → while systematically under-weighting

Management narrative, issuer disclosures, short-term metrics → while systematically under-weighting  governance issues,

governance issues,  related-party exposure,

related-party exposure,  forensic red flags,

forensic red flags,  political proximity &

political proximity &  retail vulnerability.

retail vulnerability.- Piramal Finance ratings ignore

Legacy DHFL asset quality concerns

Legacy DHFL asset quality concerns- Large wholesale/structured credit exposures

Persistent governance & recovery opacity

Persistent governance & recovery opacity

History repeats pattern IL&FS, Yes Bank, DHFL — all retained investment-grade ratings almost until collapse → massive public losses.

History repeats pattern IL&FS, Yes Bank, DHFL — all retained investment-grade ratings almost until collapse → massive public losses. High ratings = powerful enabler →

High ratings = powerful enabler →  lower borrowing costs (50–80 bps advantage) →

lower borrowing costs (50–80 bps advantage) →  rapid debt growth (~₹75,000 Cr borrowings) →

rapid debt growth (~₹75,000 Cr borrowings) →  aggressive retail deposit mobilisation → wider participation by mutual funds, insurers & retail investors

aggressive retail deposit mobilisation → wider participation by mutual funds, insurers & retail investors DHFL acquisition – the original sin

DHFL acquisition – the original sin Acquired ₹90,000+ Cr loan book for ₹37,250 Cr

Acquired ₹90,000+ Cr loan book for ₹37,250 Cr- Alleged ₹45,000 Cr fraud recoveries valued at Re 1

- Supreme Court upheld resolution plan despite serious NCLAT criticism, allegedly due to Piramal’s crony proximity to the BJP

~2.5 lakh retail FD holders (mostly senior citizens) suffered 55–77% haircuts

~2.5 lakh retail FD holders (mostly senior citizens) suffered 55–77% haircuts

- Massive asymmetric risk transfer Losses → households & retail depositors Upside & future recoveries → Piramal Group

Wider governance & controversy red flags (routinely ignored by agencies)

Wider governance & controversy red flags (routinely ignored by agencies)- Multiple SEBI insider trading actions & settlements

NGT pollution notices

NGT pollution notices ED probe (₹2,000 Cr Omkar loan)

ED probe (₹2,000 Cr Omkar loan) Alleged one-sided real-estate contracts

Alleged one-sided real-estate contracts Frequent mergers/demergers criticised for liability obfuscation

Frequent mergers/demergers criticised for liability obfuscation- Very high political proximity (electoral bonds ~₹85 Cr+ to the BJP, ₹25 Cr opaque PM CARES donations, highly controversial Flashnet deal linked to BJP Minister Piyush Goyal family, also secondary kin of Mukesh Ambani, BJP’s favoured corporate magnate)

Backdoor listing (Nov 2025) Reverse merger of Piramal Enterprises into Piramal Finance → avoided rigorous IPO scrutiny & fresh disclosures →

Backdoor listing (Nov 2025) Reverse merger of Piramal Enterprises into Piramal Finance → avoided rigorous IPO scrutiny & fresh disclosures →  absorbed contested DHFL legacy into listed entity while disowning past liabilities through shrewd rebranding→ quickly achieved ₹36,000+ Cr market cap on momentum

absorbed contested DHFL legacy into listed entity while disowning past liabilities through shrewd rebranding→ quickly achieved ₹36,000+ Cr market cap on momentum What ratings structurally miss Related-party evergreening • fraud/forensic risk • political/regulatory proximity • cyclical wholesale credit risk • severe retail depositor impact in resolution

What ratings structurally miss Related-party evergreening • fraud/forensic risk • political/regulatory proximity • cyclical wholesale credit risk • severe retail depositor impact in resolution- Risk exposure by investor type

- Shareholders → provisioning, regulatory & reputational shocks ahead

Bondholders/institutions → principal not assured in downturns

Bondholders/institutions → principal not assured in downturns- Fixed deposit holders → high-yield trap; history shows depositors bear maximum loss

- Mutual fund investors → hidden contagion risk through debt & structured products

- Systemic failure, not one-off case When rating agencies defer to issuers, regulators prioritise continuity, and markets treat ratings as truth → trust becomes a commercial product, losses get socialised, gains privatised.

Your Bottom Line & Call to Action

Your Bottom Line & Call to Action

Ratings are a paid opinion — not a safety guarantee.

Ratings are a paid opinion — not a safety guarantee.

Before investing in Piramal Finance instruments, you must:

Study the DHFL resolution & retail haircuts

Study the DHFL resolution & retail haircuts- Examine the full governance controversy list

- Review independent forensic & investigative reports

Question whether real risks are actually priced in

Question whether real risks are actually priced in Ask: whose interests do these ratings really serve?

Ask: whose interests do these ratings really serve?

Demand now:

Full transparency on legacy assets, fraud recoveries & stress tests

Full transparency on legacy assets, fraud recoveries & stress tests Real reform of credit rating industry (end issuer-pays, mandate forensic audits)

Real reform of credit rating industry (end issuer-pays, mandate forensic audits) Much higher regulatory scepticism towards legacy-heavy NBFCs

Much higher regulatory scepticism towards legacy-heavy NBFCs

Your money deserves truth — not engineered confidence.

Scepticism in such an environment is not cynicism. It is investor responsibility.

Spread awareness. Protect your savings. Demand better before the next DHFL happens.

Spread awareness. Protect your savings. Demand better before the next DHFL happens.

Public Interest Directive to Investors and Market Participants

This document is not meant to be read in silence.

If you are a shareholder, bondholder, fixed-deposit holder, mutual fund investor, pensioner, or concerned citizen, you are urged to circulate, archive, and amplify this analysis across the fifth pillar of contemporary democracy: digital media.

In a system where institutional gatekeepers have failed, public memory and digital dissemination are acts of market self-defence. Transparency today does not emerge from regulators alone; it survives through collective vigilance, networked scrutiny, and refusal to forget.

Read. Verify. Share. Question. Preserve.

Do not allow manufactured trust to outpace public truth.

SEE MORE:

Comments

Post a Comment